Production

The process by which a producer takes inputs (factors of production) and creates an output

Fixed Costs

The costs that aren’t affected by the quantity produced

Examples:

Rent

Variable Costs

The costs that are affected by the quantity produced

Examples:

Tomatoes to make pizza sauce

Total Revenue

Total amount of money a firm brings in

TR = P * Q

Accounting Profit

The amount of money a business makes

Just explicit costs

Economic Profit

Profit, including the opportunity cost

Explicit and implicit costs

Total Product (TP)

How much a firm outputs in total

Example: 2 workers produce 50 units, total is 50

Average Product (AP)

Divides total product by number of inputs

Example: 2 workers produce 50 units, average is 25

Marginal Product (MP)

Additional output from adding one more input

Helps us determine when we should stop adding more inputs - zero or negative, we stop

Example: 2 workers produce 50 units, 3 workers produce 60 units - the 3rd worker’s MP was 10 units

Law of Diminishing Marginal Product

As we add more inputs, the additional product produced we get from each input will eventually diminish

Returns to Scale

Proportional increase in output from an increase in inputs

Production doubles when input doubles

Increasing Returns to Scale

Production more than doubles with doubled input

Decreasing Returns to Scale

Production less than doubles with doubled input

Short-Run

Period of time where at least one input is fixed and cannot change

Long-Run

Period of time where no variables are fixed

Accounting Costs

Explicit costs paid by firms to use resources during the production process

Economic Costs

Sum of both the implicit costs (opportunity costs) and explicit costs of production

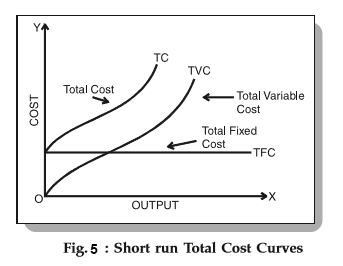

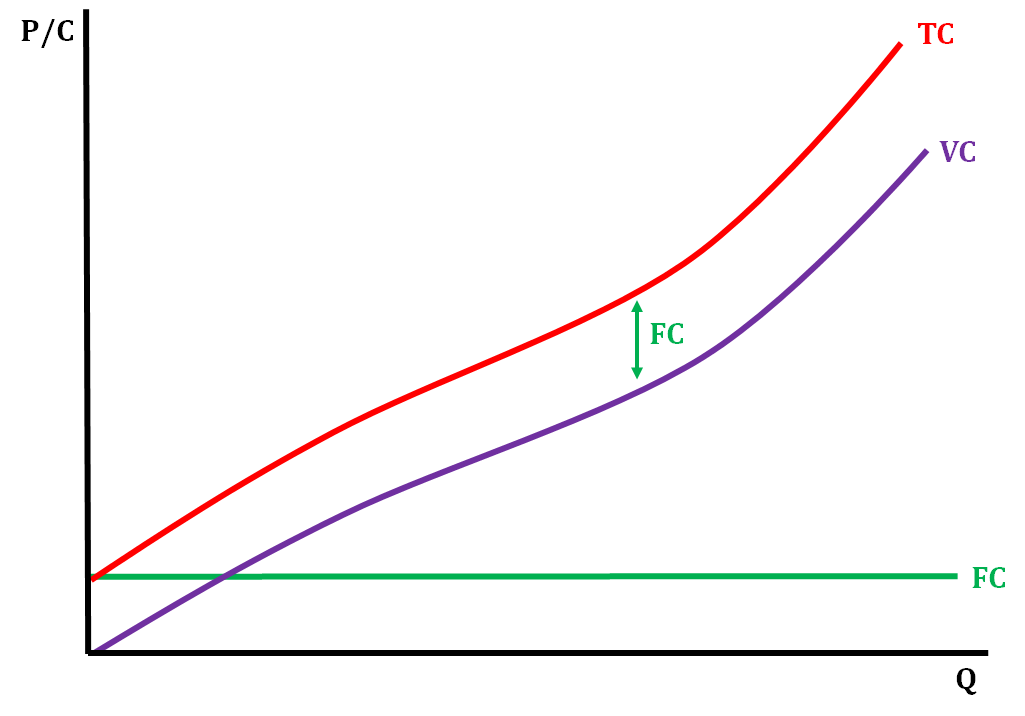

Total Cost

Total cost of producing some quantity of output

Sum of the variable and fixed costs

TC = VC + FC

Cost Curves Graph

Profit

Difference of revenue and costs

Profit = TR - TC

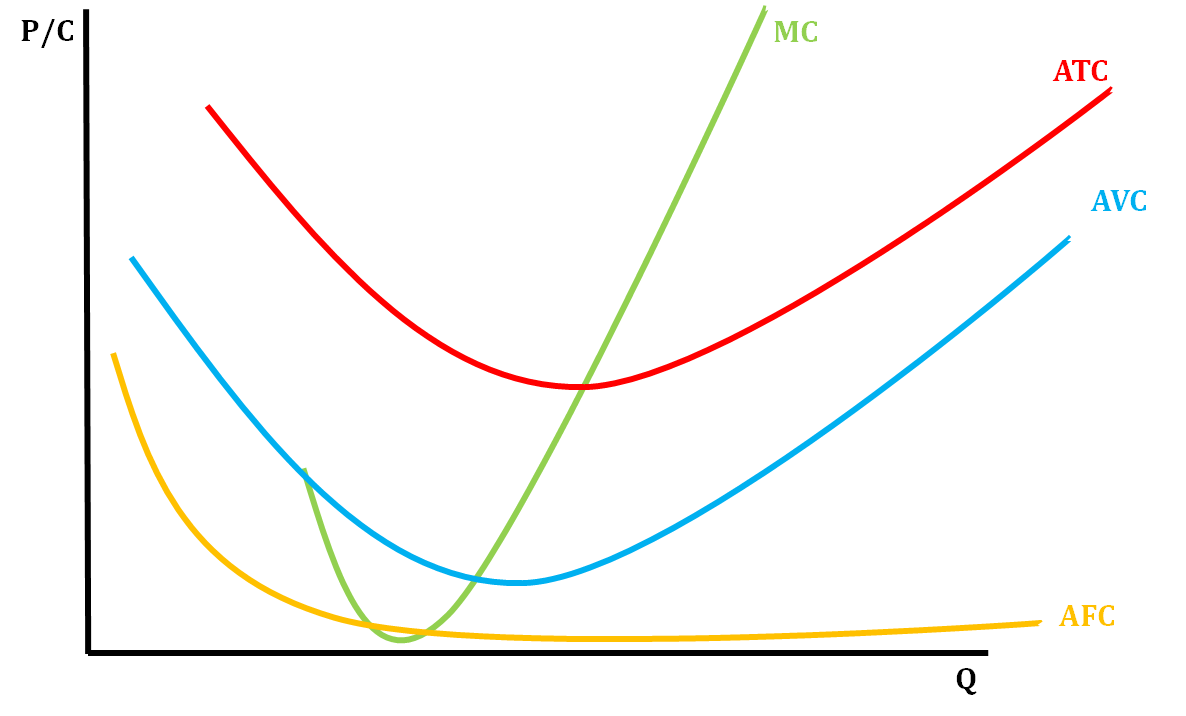

Average Total Cost (ATC) Equation

TC / Q

AFC + AVC

Average Variable Cost (AVC) Equation

VC / Q

ATC - AFC

Average Fixed Cost (AFC) Equation

FC / Q

ATC - AVC

Marginal Cost

Additional cost of producing one more unit

Total Cost, Variable Cost, Fixed Cost curves

MC, ATC, AVC, AFC curves

In the long run, all resources are…

flexible

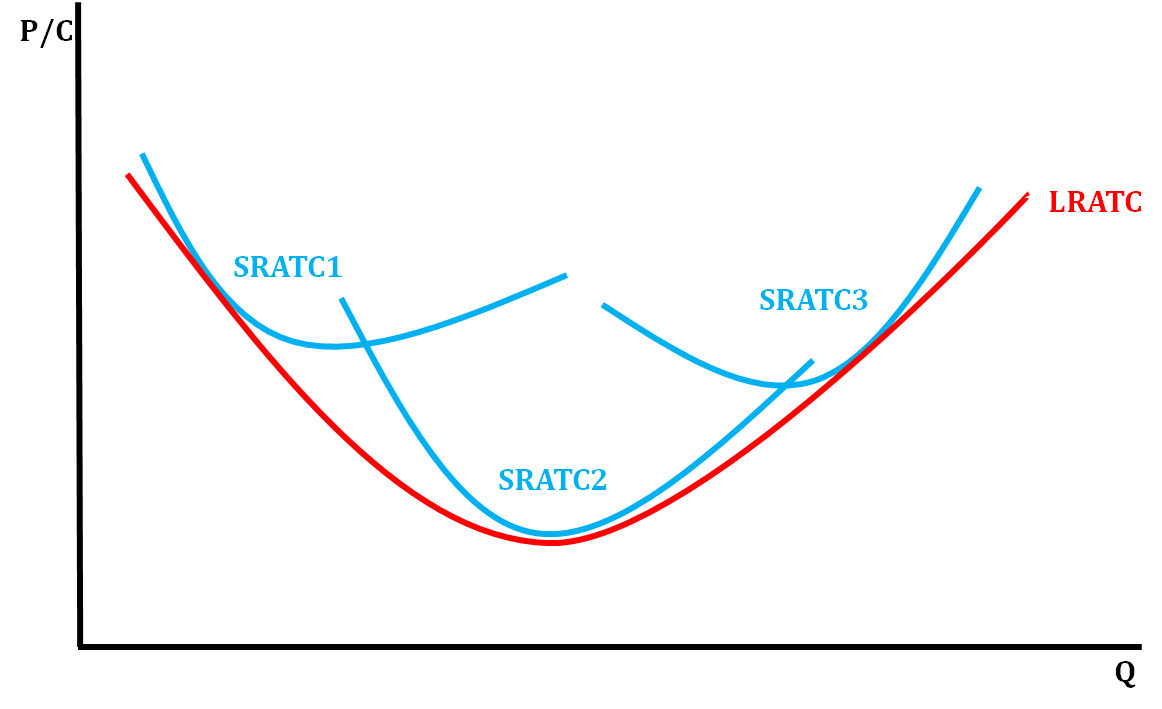

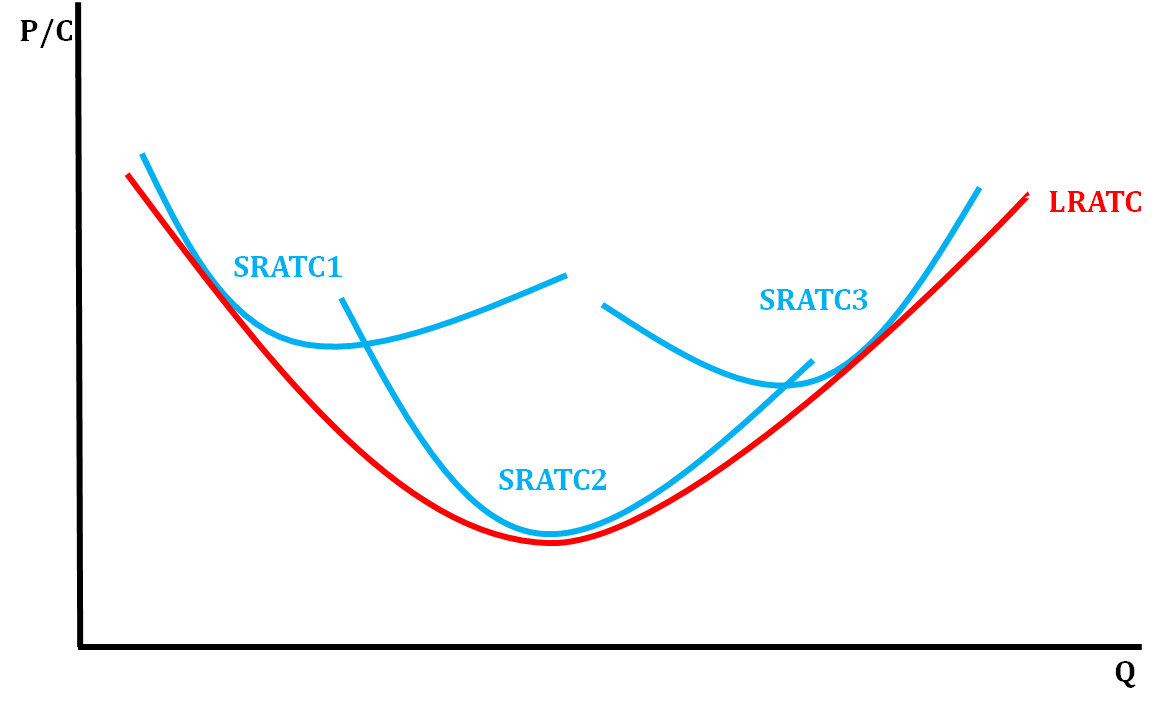

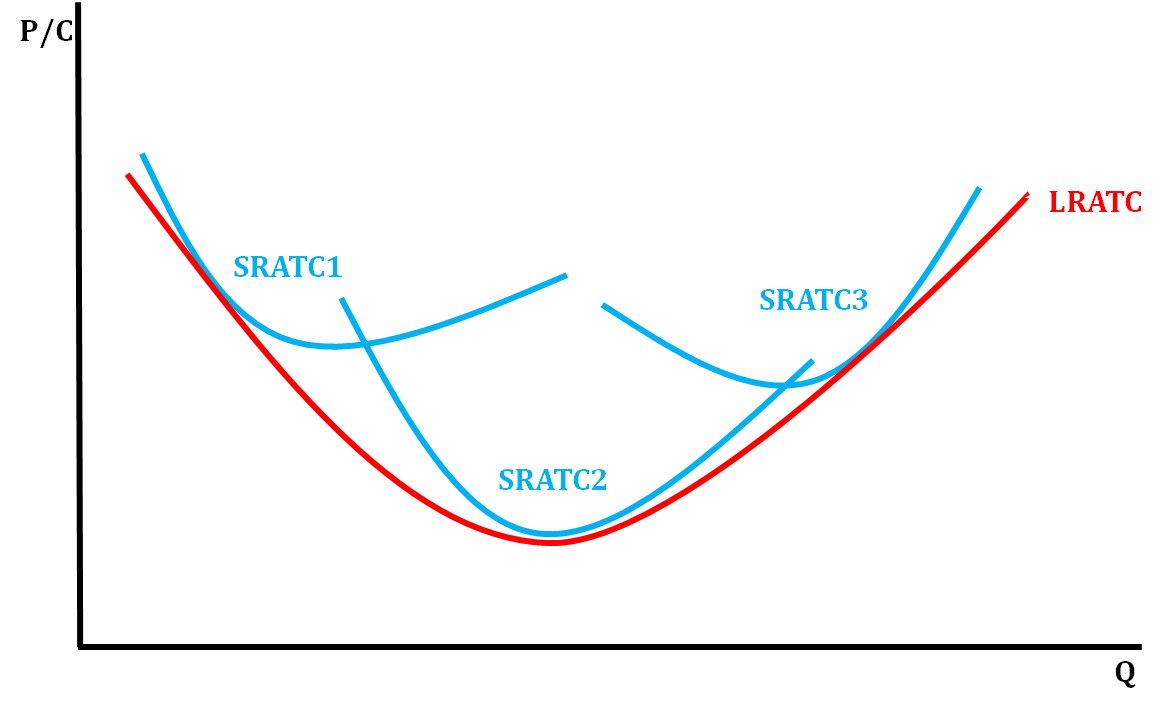

Long Run ATC (LRATC) Curve

Short Run Total Cost Curves will shift in the Long Run as more is produced

How do we find Long Run ATC (LRATC)?

Take the lowest average total cost curve at each level of output (short run cost curves)

LR ATC Car Scenario (to help understand)

In the beginning of production, a factory does not use it’s full plant capacity and mass production is difficult, so there is a high cost producing less quantity

As the firm continues production, it expands in capacity and can mass produce, lowering ATC

As the firm expands, its output becomes larger than its plant capacity and is too big to manage, so costs rise again

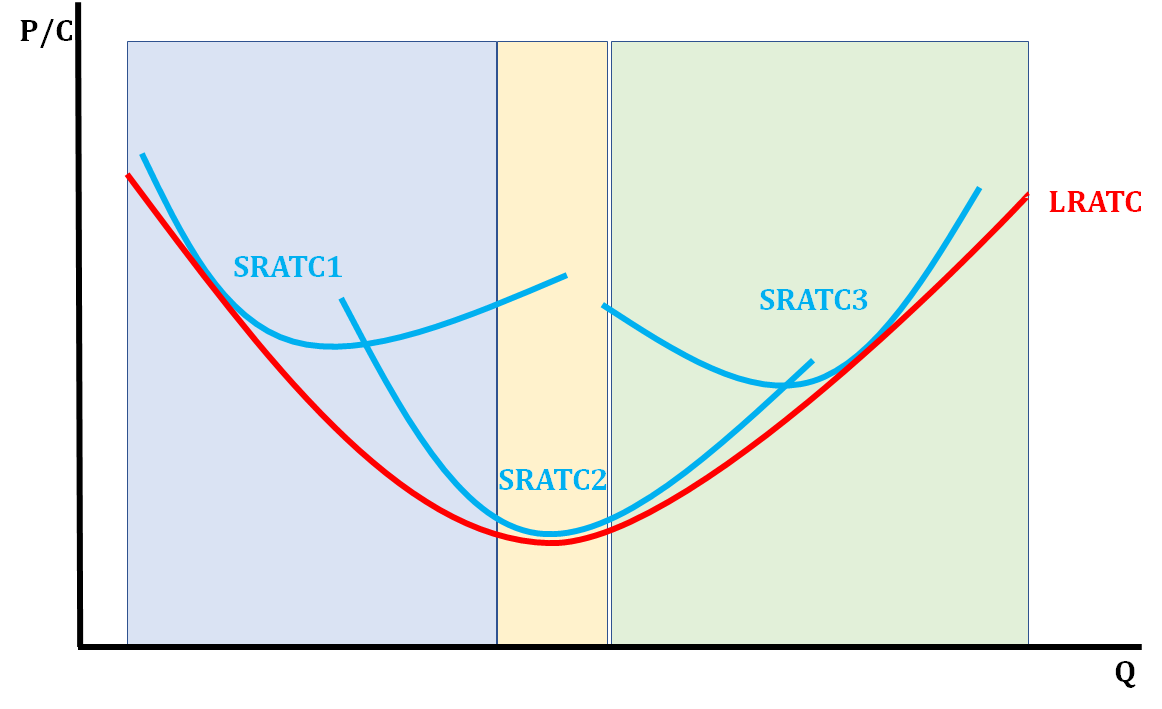

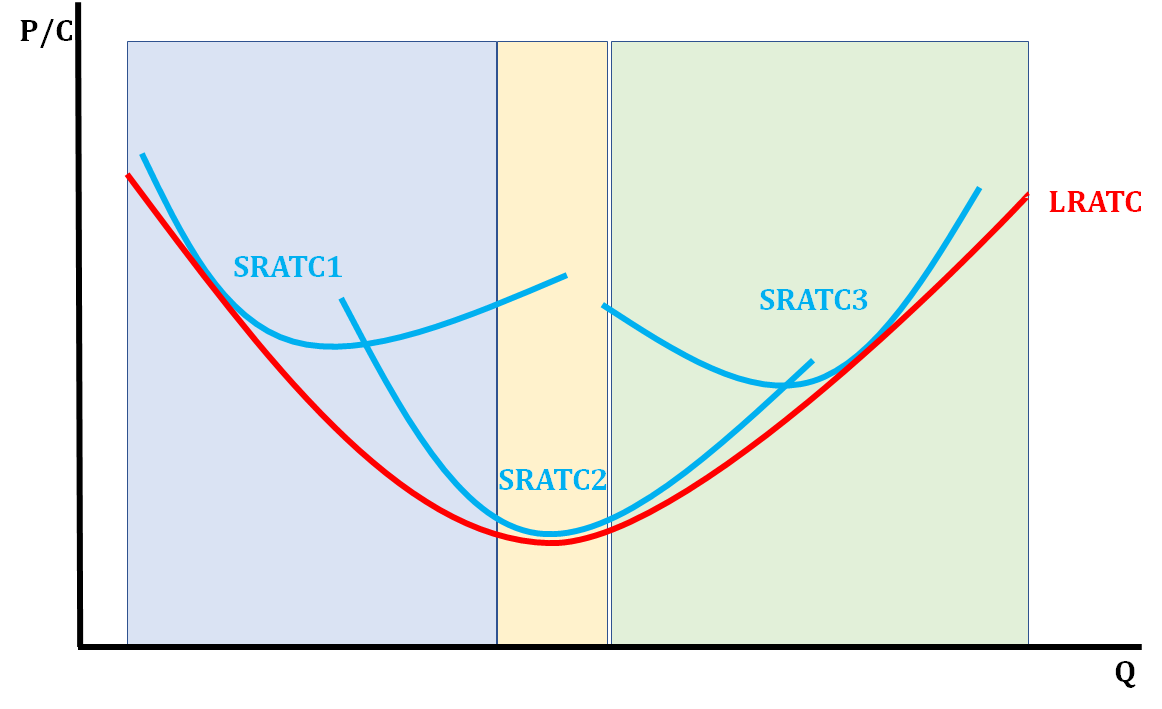

Economies of Scale

Refers to the reduction in total cost-per-unit as a firm increases its production

In this phase, the firm can reduce the total cost-per-unit by boosting its plant capacity and output

Diseconomies of Scale

Refers to the rise in total cost-per-unit as the firm increases its production

In this phase, the firm would be better off reducing its plant capacity and output to lower per-unit costs

Constant Returns to Scale

Between Economies of Scale and Diseconomies of Scale

In this phase, when the firm increases production, costs stay the same

ATC is at its lowest

Economies/Diseconomies of Scale

Blue is Economies of Scale

Green is Diseconomies of Scale

Yellow is Constant Returns to Scale

What does each color represent in the graph:

Blue

Yellow

Green

Blue = Economies of Scale

Yellow = Constant Returns to Scale

Green = Diseconomies of Scale

Normal Profit

When economic profit is zero - breaking even

Our accounting profit is positive

Economic losses

When revenue is less than costs

Supernormal profit

When a firm experiences economic profits in the long run

Theory of the Firm

The primary goal of any firm, regardless of market structure, is to maximize profits

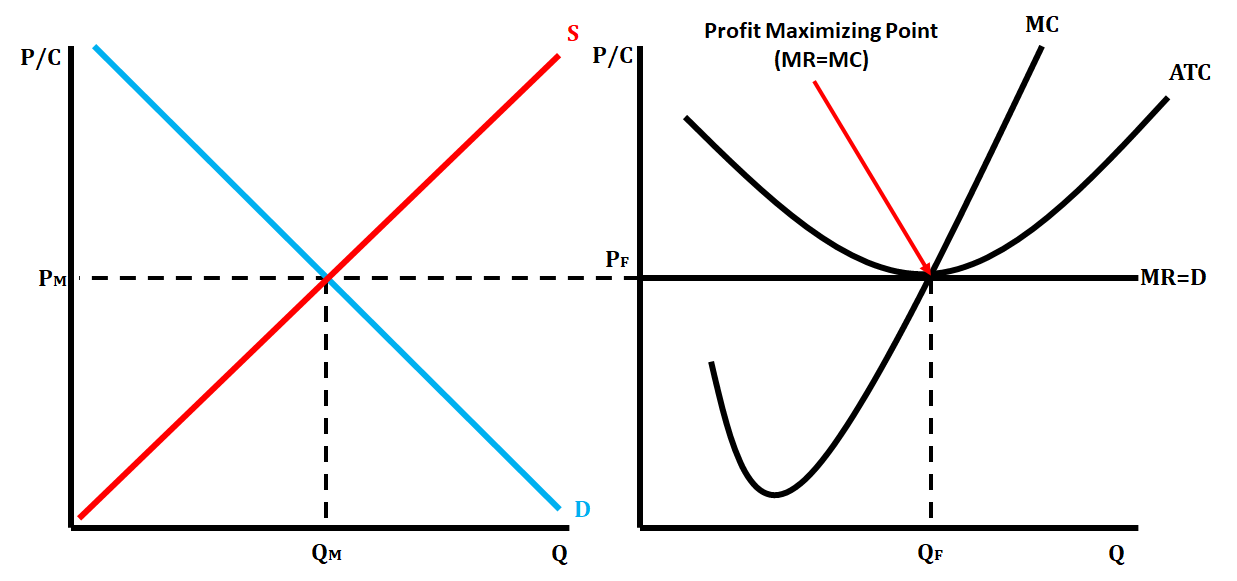

Profit Maximizing Rule

MR=MC

Perfectly Competitive Market

Many, small firms in the industry

Firms are price takers, and have no control over the price of the goods they sell in the market

Market is impacted when firms enter or exit

Low barriers to entry

Firms break even in the long run

Products sold are identical

No non-price competition

All products are identical, so no need for advertising

Firms are perfectly efficient in the long-run

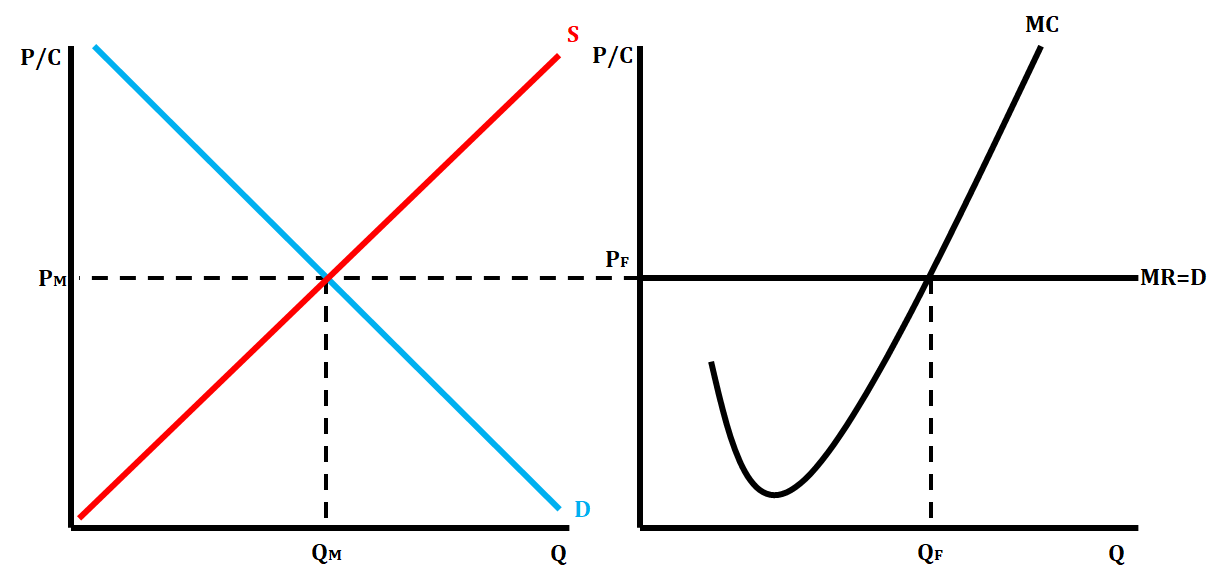

Perfect Competition Side by Side Graphs

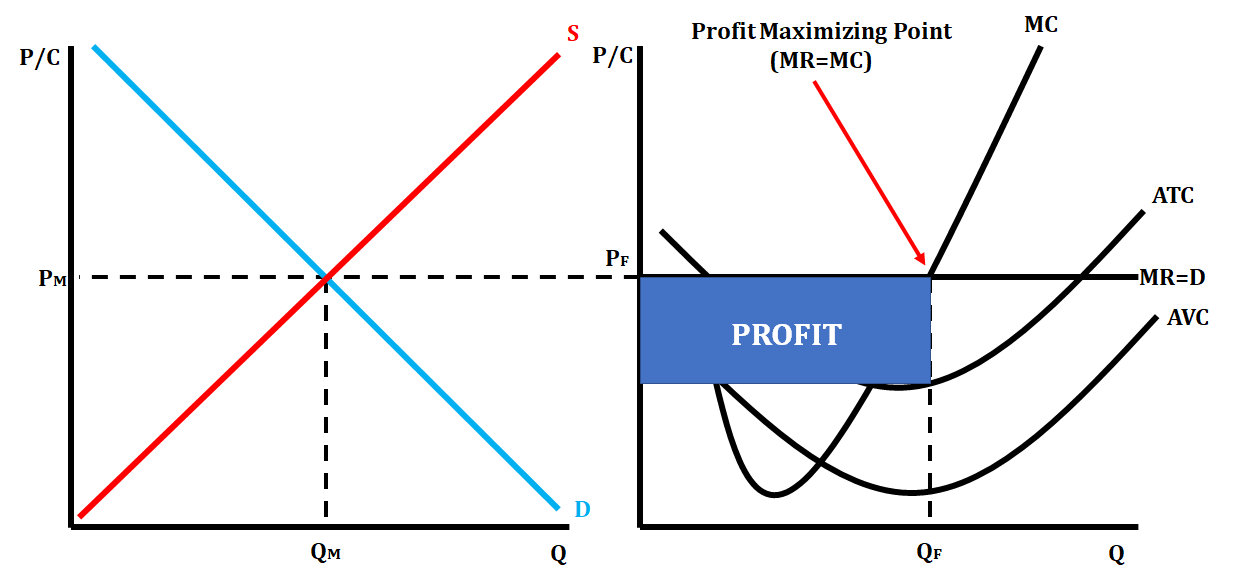

Perfect Competition Short Run Profit

ATC and AVC curves are below MR=MC

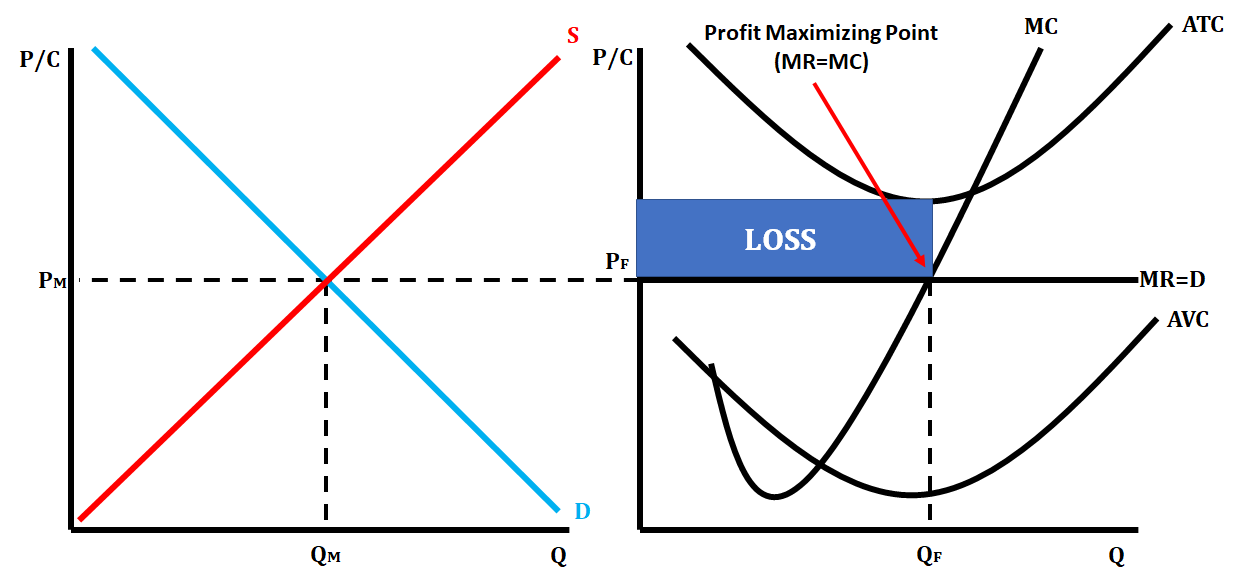

Perfect Competition Short Run Loss

ATC curve is above MR=MC, and AVC curve is below MR=MC

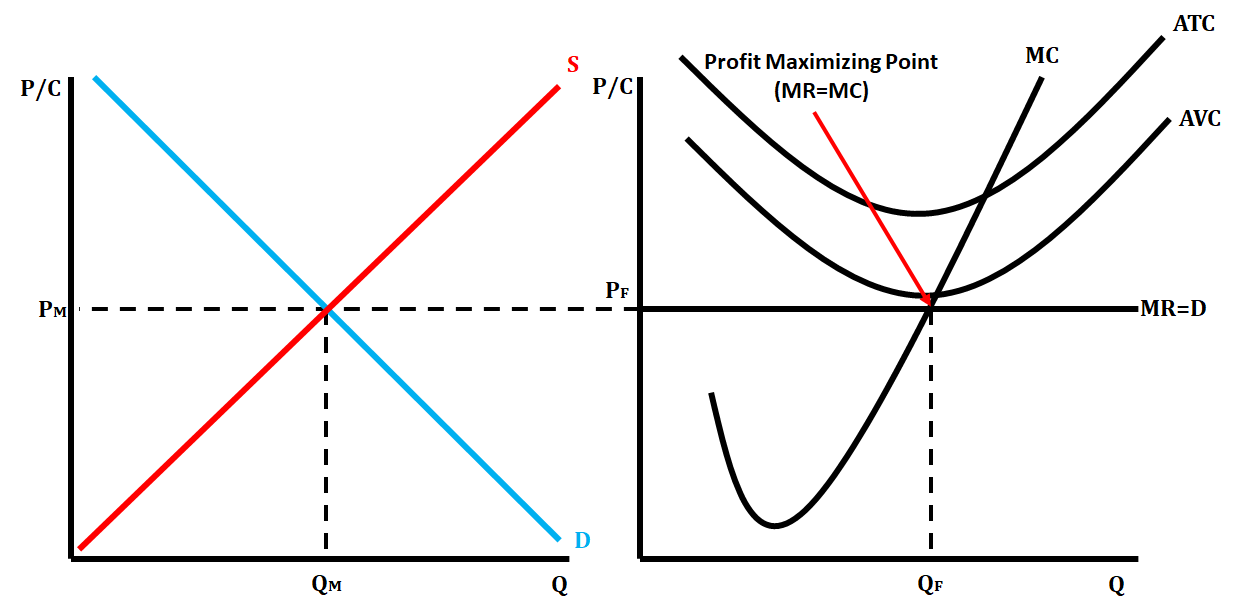

Perfect Competition Short Run Shut Down

ATC and AVC curves are above MR=MC

Perfect Competition Long Run Equilibrium

ATC Curve is tangent to MR=DARP where MR=MC

It is allocatively and productively efficient - perfectly efficient

Perfectly Competitive Market

Short Run Shut Down Rule

The firm should continue to operate as long as the price is equal to or above AVC

Perfectly Competitive Market

When firms are earning economic loss in the short run, in the long run firms will…

leave the industry due to the lack of profit available

Perfectly Competitive Market

When firms are earning economic profit in the short run, in the long run firms will…

enter the industry due to the potential profit available

What is MR DARP?

MR = D = AR = P

Market equilibrium is equal to marginal revenue

Perfectly Competitive Market

When a firm enters the market, what will happen?

Supply will shift right

This will decrease price, driving MR DARP down

Perfectly Competitive Market

When a firm leaves the market, what will happen?

Supply will shift left

This will increase price, raising MR DARP up

Perfectly Competitive Market

In the long run, the market will shift towards…

equilibrium, or normal profits