What are the factors of production?

Land, Labor, Capital, Entrepenuership

What are goods

tangible objects

What are services

actions one person performs for another, intangible

What is capital

Man made resource that is used to produce goods/services

What are the 9 key concepts

Scarcity, Efficency, Choice, Government Intervention, Economic well-being, Sustainibility, Equity, Change, Interdependance

Scarcity

Resources are scarce, not all wants/needs can be fulfilled.

What is Demand

Quantity of a good/service that consumers are willing and able to purchase at a willing price at a willing time period

Law of Demand

As a price of the product falls, quantity demand increases, ceteris paribus (held constant)

Income effect

Higher = more demand

Lower = less demand

Substitution effect

As the price of the normal good rises (+ demand falls), the price of the inferior good rises (+ higher demand), ceteris paribus.

What curve is this?

Demand curve

Market demand

Sum of all individual demands for a good/service equal to the total quantity demanded by all consumers at a given price

What are the non price determinants of demand?

Changes in income, tastes and preferences, Change in the price of substitute + complimentary goods (related goods), change in the number of consumers, future price expectation

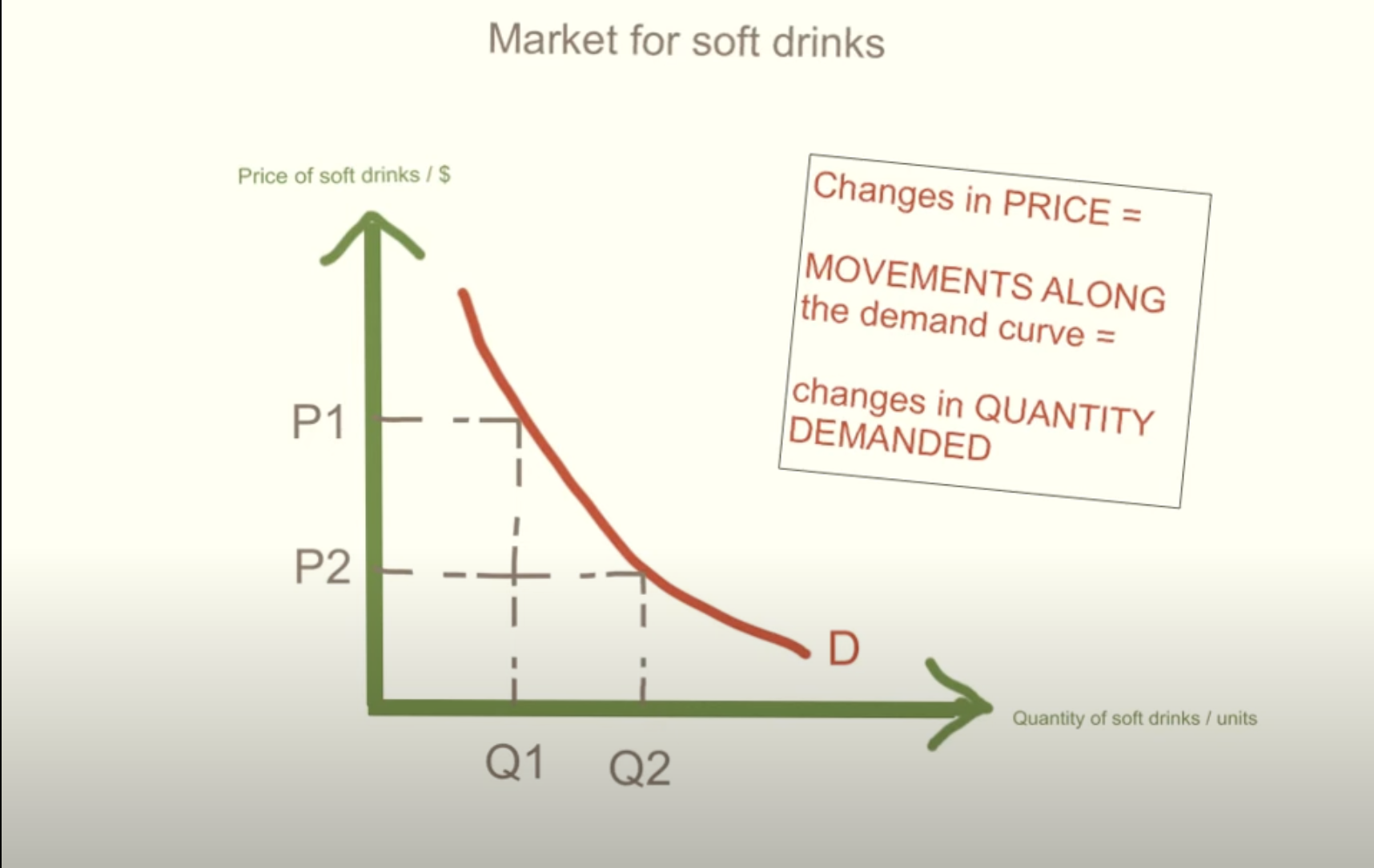

Movements along the demand curve

Changes in price, quantity demanded is constant

Shift in the demand curve

Changes in factors like income and others shift left/right, price+demand increases or decreases

Supply

Quantity of a good/service that produces are WILLING and ABLE to supply at a given price point at a given time

Law of Supply

As the price of a product rises, the quantity supplied of the product will rise, ceteris paribus

Higher prices

Higher profits, increase in quantity, more producer competition in market

Lower prices

Lower profits, decrease in quantity, more producer competition in market

Market supply

Sum of all individual producers supply at a given price at a given time

Movement along the supply curve

Price shifts up, quantity increases

Changes in price

Shifts of the supply curve

Increase in supply = right

Decrease in supply = left

Price + Quantity increase/decrease together

Cost in the factors of productions

Same as regular, except wages, rent, interest, profits

Non price determinants of supply

Changes in technology, changes in the price of related goods, change in producer expectations, change in indirect taxes/subsidies, number of firms in the market

Joint supply

goods often produced together (ex: lamb/wool)

Competitive supply

goods that are alt factors of the same factors of production (

Indirect tax

taxes on production/expenditure paid for by the consumer, and producers pay them to the government

subsidy

sum of money given to producers by the government per unit of output, shifts to the right. reduces the cost of producing a good

PED

responsiveness of quality demanded to a change in price along a given demand curve

PED formula

% change in quantity demanded over % change in price

Example of PED

20-35/35 × 100 = -15/35×100=-43

Perfectly Inelastic Demand

a small increase/decrease in price will have NO change on the quantity demanded or supplied

What is Perfect Inelastic Demand equal to?

0

What graph is this?

Perfect Inelastic Demand

Perfectly Elastic Demand

The quantity demanded responds infinitivly to changes in price (super sensitive, drops completely)

What is Perfect Elastic Demand equal to?

Infinite

What graph is this?

Perfectly Elastic Demand

Price In-elastic Demand

when the price goes up, consumers demand stays the same, and when it goes down, the demand stays the same (steep demand)

What graph is this

Price In-elastic Demand

Price Elastic Demand

change in quantity demanded exceeds change in P (sensitive to price changes)

What graph is this?

Price Elastic Demand

What graph is this?

Unit Elastic Demand

Unit Elastic Demand

Change in quantity demanded has a porportional change to change in price (curve)

PED > 1 is..

Price-elastic demand

PED = 1 is..

Unit elastic demand

PED < 1 is..

Price Inelastic

Determinants of Price Elasticity of Demand

Number & closeness of substitutes, porportion of income spent on the product, degree of nessecity, Time (shortrun/longrun)

Revenue

the value of income a buisness recieves from selling a good

Revenue formula

price x quantity

Demand for commodoties are..

relatively inelastic

Demand for manufactured goods are..

relatively elastic

limitations of PED

can change overtime, a number of factors can change over time even though it is held to ceteris paribus, uncertainty from consumers due to a change in price

Income elasticity of demand (YED)

responsiveness of quantity demanded to a change in household income

YED formula

% change in QD / % change in income

Normal goods (YED)

positive YED. Qd rises as income rises

Nessecity goods (YED)

YED between 0 and 1 (change in income = greater than porportional change in quantity demanded)

Luxury goods (YED)

demand has a YED greater than 1 (increase in income = greater than porportional increase in demand)

Inferior goods (YED)

negative YED because Qd falls as household incomes rise, vice versa

Determinants of PES

Time (long run = elastic, short = inelastic), avaiability of factors of production, stock and used capacity

Price Elasticity of Supply (PES)

responsiveness of the quantity supplied of a good to a change in price

Price elastic supply

greater than 1. Change in price leads to porportional change in supply

Unitary Elasticity of Supply

equal to 1, porportional equal change in Qs and change in price

Price Inelastic supply

less than 1 , change in price leads to less poportional change in quantity supplied

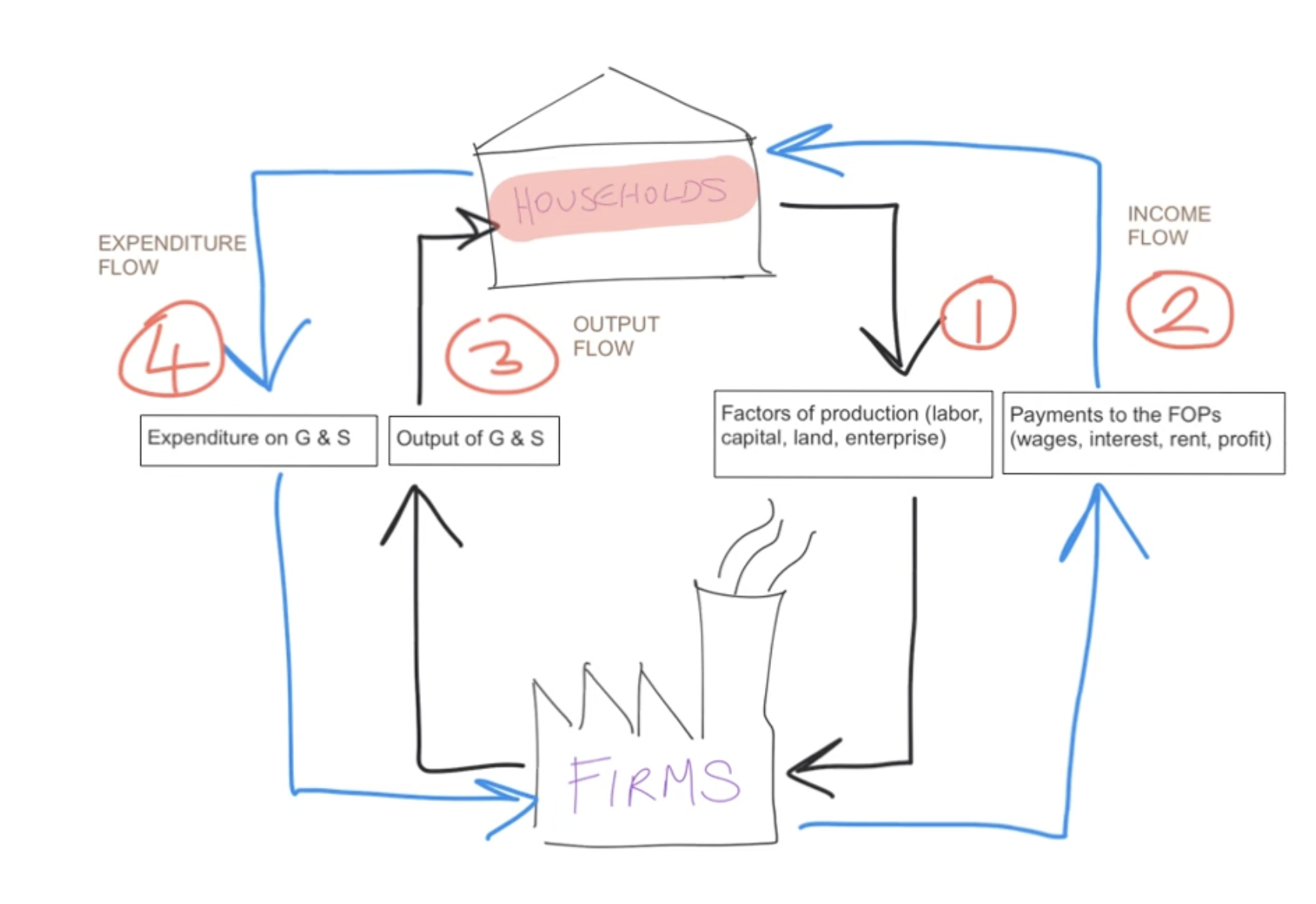

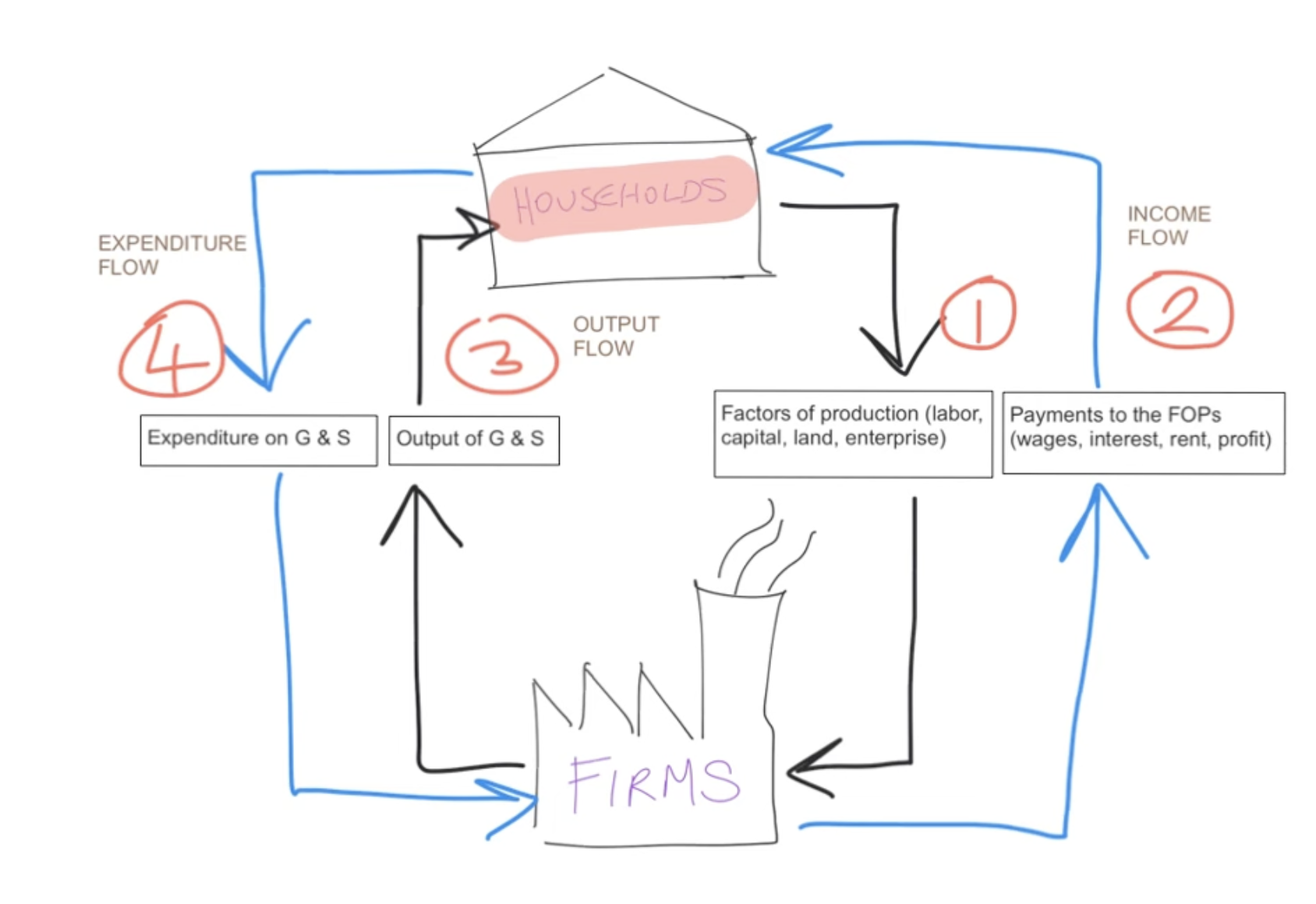

What model is this

Circular flow of income

Assumptions for this circular flow of income

simple economy (no govt sector), closed economy (no foreign sector + imports/exports), households can spend (no financial markets, investment)

Circular flow of income

model that illustrates the flow of money between households and firms

Direct Tax

Taxes imposed on income, affect demand bc they reduce income

2 types of Indirect Taxes

Specific and Ad Valorem

Ad Valorem

fixed percentage tax added to the price of a good/service such as VAT

Specific Tax

set money of tax added to price of goods such as petrol alc and cigarettes

Why are indirect taxes placed

To collect government revenue

To reduce consumption of goods they think have significant social costs

Reasons for subsidies

Some goods increase social benefits and consumption increases welfare

Used to support agriculture, steel, energy producers

Important for economic development/employment

Paid to firms to protect them from foreign comp

What does PES/PED affect (Subsidy)

The amount paid by the government and benefits paid to consumer/producer

Size of welfare loss of the subsidy

Consumer subsidy impact

Fall in price, so increase in consumer surplus

Producer subsidy impact

gain in producer surplus and revenue

best benefit at producers who can’t survive without a subsidy

Government subsidy impact

Oppotournity cost for the government from other areas of govt expenditure

May have to raise taxes to pay for subsidy

Cost in terms of managing/distributing

Welfare loss

occurs when there’s an inefficent use of resources in a market

Maximum price/price ceiling

price set by the government/authority to prevent the price of a good or service from rising above a fixed level

Reasons for maximum price

To protect low income consumers from prices rising that they cannot afford

Normally put on goods that the government feels that all people ought to be able to consume like healthcare, education, basic food

Consequences of price ceiling

Creates shortages or excess demand

Inefficent allocation of resource

Welfare impacts and dead weight loss

Buyers paying, then reselling illegally in the black market

Price ceiling impact on consumers

those who buy the good benefit because they have to pay a lower price

gain in consumer surplus, but if they cant buy the good at max price there is loss

some consumers have to enter the parallel market and risk getting in trouble

Price ceiling impact on producers

loss of producer surplus when there is a max price, recieving less revenue/profit

some leave the market and producer surplus disappears’

some producers enter the parallel market and profit there

Price ceiling impact on governments

the cost of setting up and enforcing price

could be political benefits from setting a price ceiling because it can reduce prices

Price ceiling impact on welfare

Max prices lead to a loss of welfare bc of loss of consumer surplus

Welfare loss of producer surplus from producers who leave the market

How can governments correct shortage

Subsiziding production

Making the good itself

Using up previously stored inventory

Oppotournity cost

Minimum price/price floor

lower limit set by governments/authority to stop the price of a good/service from falling below a level

Reasons for min prices

To raise income of producers esp agricultural

To protect workers by setting min wage