Tags & Description

Identify the reasons why our money has value

It is accepted by other people for goods and services.

It holds it’s value, stability with predictable levels of inflations

Describe functions of money

Medium of exchange

Store of Value

Unit of accounting

Explain the definitions of money used in the U.S. (M1, M2)

M1 = physical money (cash and coins), checkable deposits (aka demand deposits or checking accounts), travelers checks

M2= M! + savings accounts, money market accounts, time deposits under $100,000.

M3= M2 + time deposits over $100,000.

Explain the concept of near monies

M2 and M3 are both near monies because they have a definite intrinsic value but cannot be immediately spent, must be liquidated to spend.

Benefit is better interest growth.

Define the variables in the equation of exchange. (MV = PQ)

MV = PQ (both must be equivalent to eachother)

M = money supply (M1)

V = velocity of money, how many times a dollar moves in the economy

P = average price level

Q = Quantity of output of all goods and services

Explain how changes in the money supply are translated into changes in nominal GDP, prices and output.

When money supply grows, interest rates drop, investment and consumption go up (AD)

When AD increases GDP, Price, and Output all go up. Reserve effect of AD decreases

Explain the fractional reserve system (how banks “create money”)

When money is deposited to banks they lend a portion of it out (excess funds) and hold a portion to be available to cover withdrawals (required reserves)

This occurs over and over effectively multiplying the amount of money deposited.

Explain the process by which banks create or destroy money and the factors that affect the increase or decrease in the money supply

By holding onto money as reserves and not lending it, its not multiplied out

Banks can also purchase treasury securities (bonds) from the Fed which also takes money out of the supply. Works in reverse too.

Define the required reserve ratio, required reserves, excess reserves, and deposit expansion multiplier

Required Reserves Ratio: % of every dollar a bank must hold and not lend

Required Reserve: Amount of money held that cannot be lent

Excess Reserve: Amount of money that can be lent out

Deposit Expansion Multiplier: 1/RR is the expected amount of money to be grown through fractional reserve banking

Tools of the Fed

Adjusting reserve requirement - (very powerful) but will allow for change to multiplier effect

Adjusting the Discount Rate - Interest charged to banks that borrow money from the Fed, signals to banks if it’s a good time to loan more $

Open market operations - Used often, buying and selling of government securities (bonds)

Discuss the motive for holding assets as money

Very stable in value, not increasing but also not dropping during economic downturns.

Real estate does grow over long time amounts but does occasionally drop temporarily

Identify the factors that cause the demand for money to shift and explain why the shift occurs

Changes to price levels (cost more/ less to buy stuff)

Changes to income levels

Changes to interest rates (encourage or discourage borrowing → spending)

Changes in wealth of assets

Changes in future expectations

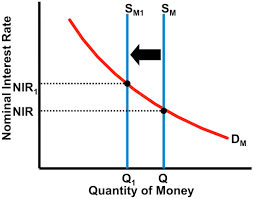

Explain how interest rates are determined in the money market

Explain how interest rates affect monetary policy

The Fed examines the economic status to try to correct problems (unemployment or inflation) then adjust the money supply to impact interest rates to stimulate or contract AD.

Explain the relationship among the real interest rate the nominal interest rate and the inflation rate. This is known as the Fisher Equation

Nominal is what we see on a daily basis in banks, there is inflation in this rate

Real excludes inflation and used on loanable funds graph by banks to determine their own interest rates

Fisher equation: Nominal Interest Rate - Inflation Rate = Real Interest Rate

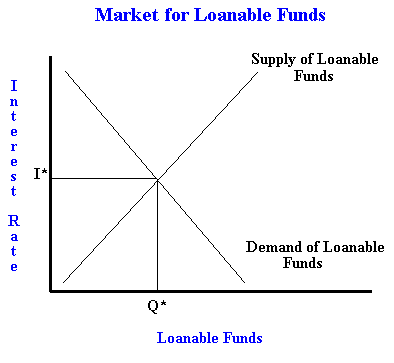

Explain loanable funds money

Used to show how bans determine the interest rates.

Bases on Supply (saver) and demand (debtors/borrowers)

Equilibrium is the interest rate

What is crowding out within loanable funds and how can monetary policy correct this

Result of expansionary FISCAL POLICY that increases interest rates (high Gov’t demand on loanable funds). Private investment drops (bad for GDP and future growth)

Expansionary Monetary (adding money into the economy) will lower the interest rates back down and encourage private investment (with cheaper interest rates)

Define Financial Sector

The part of the economy made up of institutions (like banks) that focus on pairing lenders and borrowers.

Define Assets

Any item of economic value that can be converted into cash. Something owned

Define Liabilities

A legal or financial obligation that must be paid back. Something owed

Define Liquidity

The ease in which asset can be converted into medium of exchange. Cash and money in checking accounts is very liquid. A car or a home is not.

Three Functions of Money

A Medium of Exchange -Money can easily be used to buy goods and services. Dont have to barter

Unit of Account - Money measured the value of goods and services and measures value

Store of Value - Money allows you to store purchasing power for the future

Types of Money; Commodity Money

Something that performs the function of money and has an alternative use (ex: mark in prison)

Types of Money; Fiat Money

Something used for exchange but has no other important use (ex: $20 bill)

What is the transaction demand for money?

People demand money to make everyday purchases. This is not affected by the interest rate

What is the asset demand for money?

When people demand as a liquid asset because they prefer it to other non-liquid assets like bonds

Interest rates ↑, then quantity of money demanded ______

↓

Interest rates ↓, then quantity of money demanded ______

↑

Shifters of Money Demand

Changes in prices level - Inflation requires consumer o hold more cash for financial transactions

Changes income - Sustained economic growth in the economy leads to an increase in the demand for money

Changes in taxation that affects personal investment - Government policies such as changing the capital gains tax would change the demand for money

Shifters of Money Supply

Reserve ratio- the percent of deposits that bank must hold in reserve (the % they can NOT loan out)

To increase money supply, decrease the reserve ratio

To decrease money supply, increase the reserve ratio

Discount Rate - The interest rate that the FED charges commercial banks

To increase money supply, decrease discount rate

To decrease money supply, increase discount rate

Open Market Operations - when the FED buys or sells government bonds (securities)

To increase money supply, the FED buys bonds

To decrease money supply, the FED sells bonds

Unexpected inflation causes the demand for money to _ and the interest rate to _ .

Unexpected inflation causes the demand for money to INCREASE and the interest rate to INCREASE.

If the supply of money increases, the interest rate will _ and investment will _

If the supply of money increased, the interest rate will DECREASE and investment will INCREASE

True or False: When the interest rate is high, the opportunity cost of holding money increases so the quantity of money demanded will decrease.

True

True or False: The money supply includes all assets like cash, demand deposits, bonds, and real estate.

False

True or False: Monetary policy is when the central banks changes the interest rates by changing the money supply

True

What is the Federal Reserve and what does it do?

The Fed is the central bank of the US and it regulates commercial banks and adjust the money supply to adjust interest rates to meet economic goals. This is called Monetary Policy

Money Multiplier Equation

1/ Reserve Requirement

Ex: Assume reserve requirement is .10. If the Fed buys $10 billion worht of bonds money supply will increase by $100billion

(1/.10) *10 =100

What is bond maturity?

A borrower issues a bond that must be paid back by a certain amount of time. That time is its maturity. A bond can be sold early at an agreed upon price.

Define Fractional Reserve Banking

Process where banks hold a portion of deposits in reserve and loan the rest of the money out.

Define excess reserves

The amount banks are legally free to loan out. Excess reserves and required reserves make up total reserve.

Define demand deposits

Banks deposits that can be withdrawn at anytime (ex: checking accounts)

Define Owner’s Equity

The amount of money owners have put into a company or bank. It doesn’t need to be held in reserve

Shifters of Demand for Loanable Funds

Changes in perceived business opportunities

Changes in government borrowing

Shifters of Supply for Loanable Funds

Changes in private savings behavior

Changes in public savings

Changes in foreign personal investment

Changes in expected profitability

What happens to the real interest rate if the government runs a deficit?

Demand increases so interest rate increase