Chapter 9: Wage Determination and Superstar Salaries

In the labour market, the demand and supply of labour determines worker earnings and the quantity of labour hired. Wages and other labour earnings are simply prices that are determined by the market interactions between buyers and sellers of labour.

The marginal cost of hiring a worker is the increase in costs that businesses incur from hiring the worker. This cost includes the wages paid to workers and can also include nonwage costs.

A production function shows the amount of output that can be produced with different amounts of inputs.

Total product is the total output produced at a given level of input use.

The marginal product of labour(MP) is the additional output gained from hiring an additional worker.

Law of diminishing marginal product is holding other inputs constant as additional units of an input are added to a production process, at some point increases in total production occur at a decreasing rate.

The value of the marginal product of labour is the increase in total revenue earned when the firm hires an additional worker.

Human capital is the skills and knowledge workers acquire through education, experience, and training that makes them more productive in the workforce.

Workers with more human capital also tend to be more productive.

When we determine the profit-maximizing hiring decision for a firm, we are really finding the firm's demand for labour.

Profit = Total Revenue - Total Cost.

To determine the maximum amount that a firm would be willing and able to pay a worker, think of the worker's contribution to the firm's revenue. A firm will earn profit whenever it can pay a worker less than his or her value of marginal product of labour.

Individual sellers of labour face choices about how much to work, who to work for, and how much to invest in their human capital. Economists assume that individuals make their labour supply decisions based on the goal of maximizing their utility.

The benefit of supplying labour is the utility obtained from working in a job you like, from the satisfaction of job well done, and from using earnings from work to purchase goods and services.

If the supply or demand for labour changes, the equilibrium wage and quality of labour hired will also change. On the supply side, factors that could increase the supply of labour include the costs of working, the wages that workers could earn in other labour markets, worker expectations, and the total number of workers in the labour market.

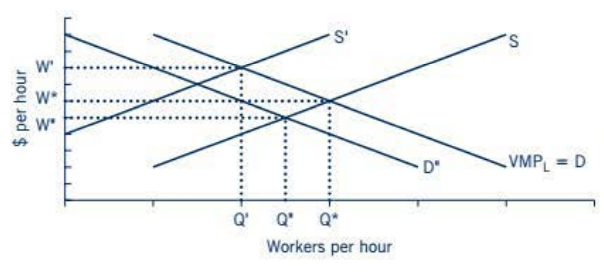

The graph below shows the number of workers a firm is willing to hire at a given wage.

At equilibrium, the wage decided is W* and the number of workers for the dedicated wage is Q* per hour.

When the price of capital falls, firms in this industry will increase the quantity of capital they demand and decrease their demand for labor.

A decrease in the demand for labor is illustrated by the movement from D to D".

When the demand for labor falls, the wage falls from W* to W" and the quantity of labor hired per hour falls from Q* to Q".

The wages that we observe in labour markets reflect the value of the marginal product of the worker hired at the margin, not the total value produced by workers in the market.

Rather than examining the wage paid to the marginal worker hired, we would more accurately determine how much society values the output of a set of workers in a particular job by adding up the VMP of all the workers in the job.