Ch 5 - Supply

Supply: the quantity of a good or service that producers are willing and able to supply at different prices in a given time period

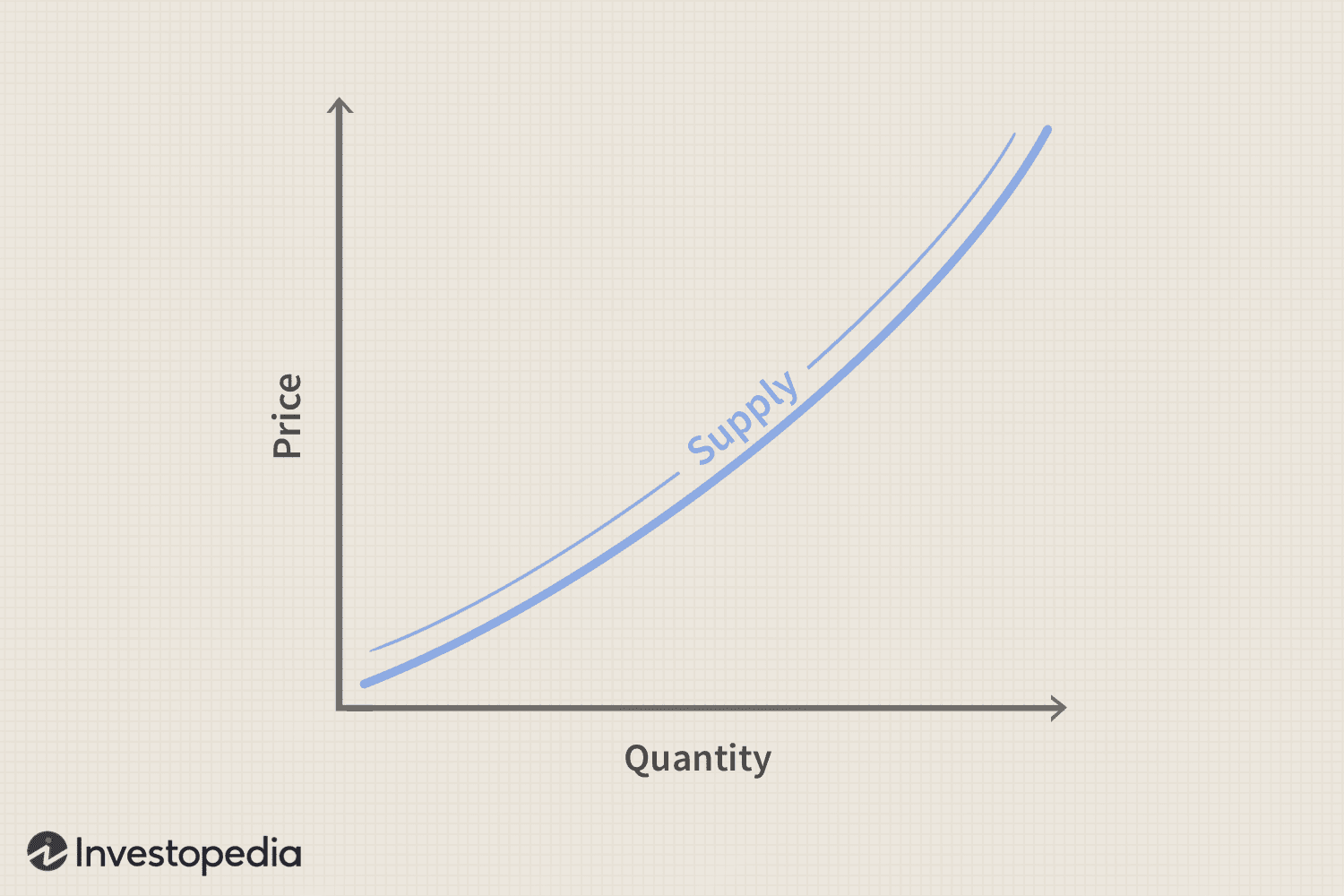

Law of supply: as the price of a product rises, the quantity supplied of the product will eventually increase

The supply curve normally slopes upwards

Price rises but costs don't change → profitability increases → supply more

Supply curve: represents the relationship between the price and the quantity supplied of a product

Non-price determinants of supply:

Changes in factors of production: (supply shifts to left) → land, labour, capital, entrepreneurship

Improvements in tech (supply shifts to the right)

Expectations: supply increases if product is expected to gain profit

Indirect taxes → increase costs → supply shifts left

Competition: if another product is produced with higher profit, supply for existing product decreases

Subsidies → reduce costs → supply shifts right

More firms → supply shifts to the right → more being supplied at each price level

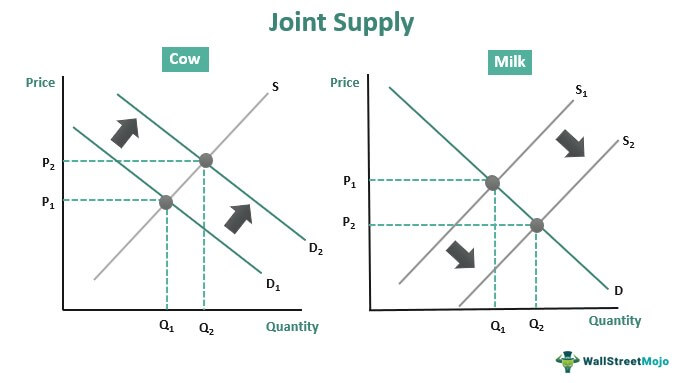

Joint supply:

The law of diminishing marginal returns: as more variable factors are added to a given quantity fixed factors, holding tech constant, marginal product eventually drops

Fixed factor: employment remains constant

Variable factor : employment increases as output increases

Short run: period with fixed + variable factors

firms can expand output by employing variable factors only

Long run: period when all factors are variable

firms can expand output by increasing the use of all factors

Marginal Product (MP): change in total product as a result of change in input

Formula: MP of the nth unit = TP of n units - TP of (n-1) units

MP = △TP /△V

Why does this happen?

Workers fully utilise fixed factors initially so MP rises

when more workers are added, too many workers relative to the amount of fixed factors, MP eventually drops

Total product: total output that a firm producers using variable and fixed factors in a given time period

Average product: output that is produced, an average, by each unit of the variable factors

Formula: AP = TPV

Rules:

As supply increases, price decreases, and demand increases

As supply decreases, price increases, and demand decreases