Unit 1 - Basic Economic Concepts Guide

Complete guide for all information relating to the basics of economic concepts

1.1 - Scarcity

Economics in general is a study of how an entity, whether it be an individual or an organization, manages and allocates its resources in the most efficient way possible. The need to allocate and organize resources is derived from the basic concept of scarcity which exists. This doesn’t just apply to money management, politics, or the stock market

The economic problem states however that our needs our unlimited and as mentioned earlier, the resources available are scarce.

In the realm of economics, all resources around us are considered to be limited; even the most basic things which exist around us like air or water

Scarcity : unlimited wants, limited resources (example : land). Where society does not enough resources to produce the goods and services which everybody needs. As a consumer, we must make choice as to how to allocate resources properly.

Microeconomics Vs. Macroeconomics

Microeconomics: filters our scope to individuals in an economy while keeping the overall economy in mind. Focuses is directed at the roles households and firms play and how their decision-making and allocation of resources impact the overall economy.

Macroeconomics: we consider the big picture- the nation’s economy as a whole. E.g. would changes to the money supply have an effect on country A’s imports and export? This branch studies the behaviour and performance of the entire economy

Factors of production

These are resources that are scarce, can be broken down into four categories:

Land: natural resources and raw material. Ex: water, oil, minerals and such.

Labor: physical labor, skills, and effort devoted into a task where workers are paid.

Capital: is usually referred to as the liquid asset, or monetary value

Physical capital: tools and equipment used to produce a good or service

Human capital: education and training an individual has that is used in the production of a good or service

Entrepreneurship: the ability of an individual to coordinate the other categories of resources to produce a good or service

Opportunity Costs and Trade-offs

Trade-offs: The alternative choice which must be given up in order to make a decision. The goods and services which you do not choose are the trade-offs.

Opportunity costs: This is the cost we forgo or sacrifice, to opt for another choice. The next best alternative if your first choice is unavailable.

Positive vs Normative Economics

The study of Economics can be broken down into 2 more ways,

Positive Economics: this approach to economics is based on facts and figures.

Theories to understand behavior are proved via a full procedure of hypothesis and testing. E.g. Increase in income for family A, increases their spending but not by the same amount as the change in income

Normative Economics: this approach to economics is based on assumptions.

Economic behaviors are first analyzed and then evaluated based on the researcher’s opinion. E.g. Refurbishment schemes can cause a decrease in the prices of second-hand phones

Both these approaches are crucial for the study of economics since economic theories are the core of our study, and theories require a hypothesis that is shaped based on what an individual feels or thinks

1.2 - Resource Allocation and Economic Systems

There are 3 big economic questions, what, how, and for whom?

What goods and services will be produced? The economy has to decide what goods and services the society needs in order to properly allocate resources.

How will goods and services be produced? This deals with how businesses will go about producing these goods and services.

For whom will the goods and services be produced? This question decides who will be able to consume these goods and services, to where these resources where will be allocated.

Types of Economic Systems

Centrally-Planned (Command) Economic System:

Here, the government makes all the economic decisions and answers the three questions on its own. They set the prices for goods and services, as well as set wage rates. However, they do not respond to consumer wants, and innovation is discouraged.

Market Economic System:

Economic changes are guided by the changes in price which occur as individuals and sellers interact in the market. There is a lot of competition and a variety of goods and services. However, there will be a wealth disparity in the market.

Mixed Economic System:

A system which has characteristics of both central system and market economic system. There are private property rights which are protected, however, the government is able to intervene in order to meet societal aims.

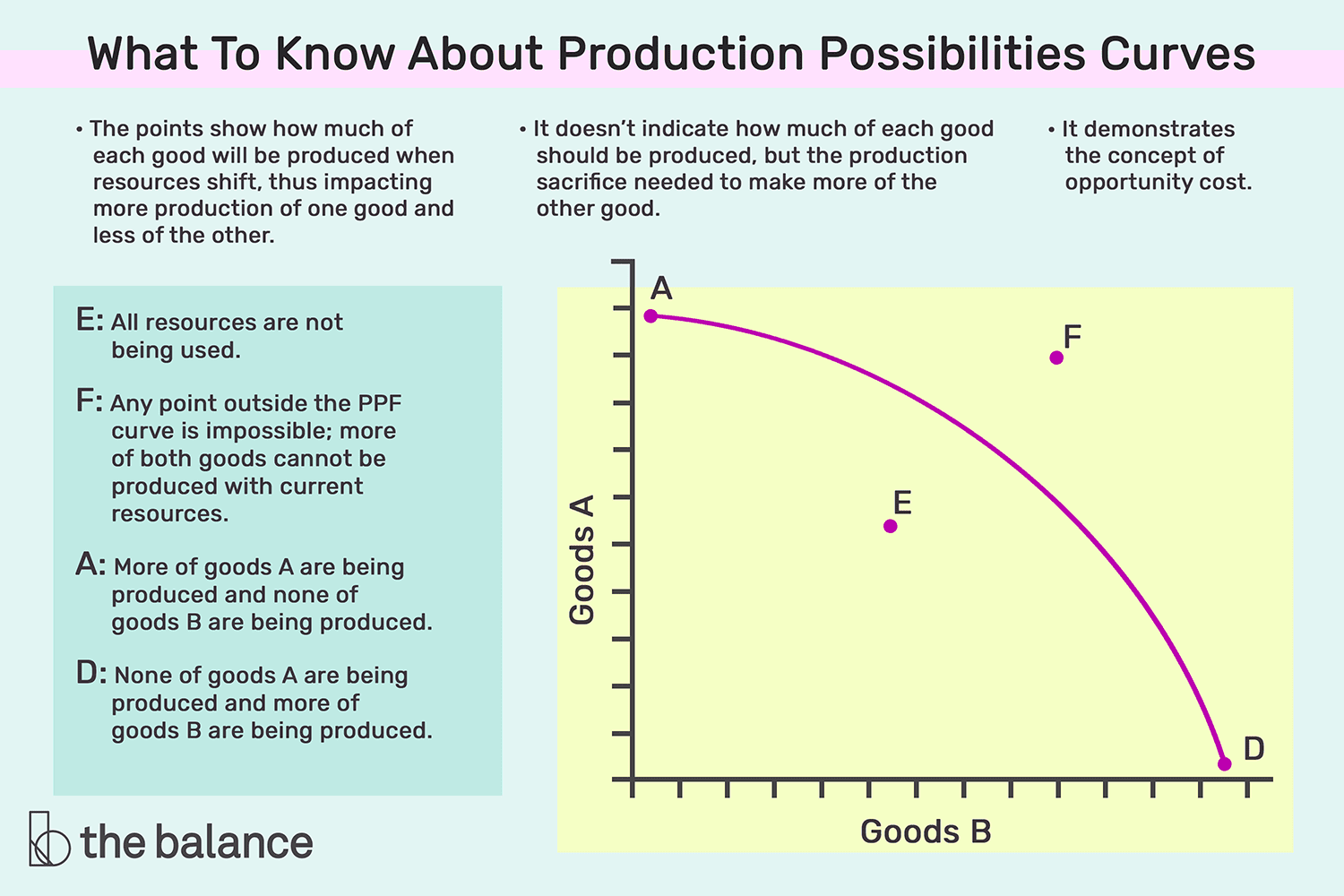

1.3 - Production Possibilities Curve

Represents the best possible combinations of goods, given a fixed amount of resources. In the graph, we can note than resources and technology is mixed, and only two goods can be made.

Illustrates the trade-offs that faces an economy, compares only two goods

If the PPC is linear, it has a constant opportunity cost, if it is curved, it has increasing opportunity costs

Economic growth : a sustained rise in aggregate output and an increase in standard of living (causes are developments in technology, or an increase in resources)

Productive efficiency : lowest cost possible on the PPC

Allocative efficiency : the economy allocates resources so consumers are well off as possible, producing what is demanded

Constant opportunity cost

Occurs when OC stays the same as the production of a good increases.

Increasing opportunity cost

When one good is produced more, you give up more of another good.

Determinants of PPC

The curve can shift upwards or downwards respectively due to certain factors:

Changes in the amount of resources in the economy:

This could be due to changes in the labor force because of population changes, acquirement of new territories (e.g. for farming, mining), or destruction of territories due to weather conditions, etc.

Changes in technology and productivity:

This could be due to government schemes to help farmers for instance or could be due to the usage of inefficient production techniques, etc

Trade:

This is dependent on new resources being discovered or improve production techniques.

1.4 - Comparative Advantage and Trade

Absolute Advantage: Occurs when a firm as the ability to produce a specific amount of goods or services in comparison to the others.

Comparative Advantage: The ability of a firm to produce a good or service at the lowest possible cost

Terms of Trade: people split up the work, and provide each other with a good in return for another. It is also the rate at which one good can be exchanged for another (if the price of a good obtained from trade is less than the opportunity cost of producing it, trade is beneficial)

Capital goods: goods that make consumer goods (ex. machinery)

Consumer goods : goods that are consumed (ex. food)

1.5 - Cost-Benefit Analysis

Implicit costs: monetary or non-monetary opportunity costs in terms of making a choice.

Explicit costs: traditional out of pocket costs which are associated with choosing one course of action.

1.6 - Marginal Analysis and Consumer Choice

Utility: the measure of personal satisfaction (util is a unit of utility)

Marginal utility: the change in total utility by consumer one additional unit of that good/service

Principle of diminishing marginal utility : additional units of a good/service add less total utility than the previous units do

Marginal utility per dollar : MUgood/Pgood (marginal utility of one unit of the good / price of one unit of the good)

Optimal consumption rule : to maximize utility, marginal utility per dollar spend on each good = service in consumption bundle, MUc/Pc = MUt/Pt