Ch 4 - Demand and Supply: The Basics

(Microeconomics)

Demand and the Law of Demand

Demand for a product is the quantity the customers are willing and able to pay for each and every price

The law of demand states that as price increases, demand for that product decreases (inverse the relationship). When the price of a product increases, the quantity demanded decreases (all other things remain unchanged) and vice versa.

The curve also helps identify what price the customers would be willing to pay

Reasons for the Law of Demand

Income effect: when prices are low, people are easily able to afford it since their budget would allow it

As prices increase, people’s budget would tend to become tighter, as they wouldn’t be willing to spend more on a product

Substitution effect: when products price increase, they tend to increase in relative to other products

If product A were to become expensive, product B would most likely be cheaper than A

Due to the existence of substitutes, customers immediately leave product A for B

Diminishing marginal utility: As more units of a product are consumed, the satisfaction/utility it provides tends to decline

Apple users would purchase at maximum, a limited phones-they wouldn’t purchase a new iPhone every month since that extra phone would offer them no utility or not as much

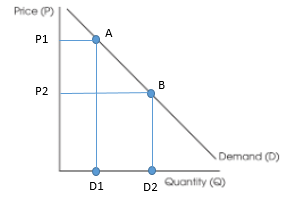

Change in Quantity Demanded vs. Change in Demand

Quantity Demanded: Has an inverse relationship with changes in the price of a particular good.

Change in the quantity demanded only occurs due to change in price-movement along the curve

If product A would become expensive(P2 to P1), the quantity demanded would fall (D2 toD1)

Changes in demand are when the entire curve would shift upwards or downwards

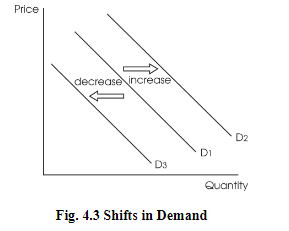

Determinants of Demand

Determinants of Demand: the factors that cause consumers to buy more or less at the same price; these are substitutes, preferences, population, income, complements, and expectations

These are the determinants of demand which are variables causing consumers to buy more or less of a product, irrespective of the price

Substitutes Available

Two goods would be considered substitutes if an increase in the price of one good causes an increase in demand for the other good

Population preference

This is the consumer’s taste for a product at any point

If consumers like a product, the demand curve for that product shifts upwards and vice versa if they dislike it

A good example is when the trend of vegetarianism hit the public, the consumption of plant-based food drastically increased

Population/number of consumers

The bigger the market for a product, the more likely the demand curve would shift upwards

If country A has a low birth rate in a particular year, the demand curve for baby-related products would shift downwards

Income

Goods are usually categorized into 2 types, inferior and normal

Demand tends to decline (shift downwards) for inferior goods with an increase in consumer income

Demand for normal goods increases (shifts upwards) with an increase in consumer income

Complementary good

These goods are purchased separately but used together. The relation here is inverse of that of substitute goods

If two products are substitutes, an increase in the price of one good causes demand for the other good to decline as well

Expectation

Consumer expectation pays a major role in the determination of the price

if consumers expect that the price of something would increase in the future, they would buy the product at a larger scale leading to the demand curve shifting upwards

A good example would be when government warns of the possible chances of future inflation, leading to people stocking up on goods at their homes

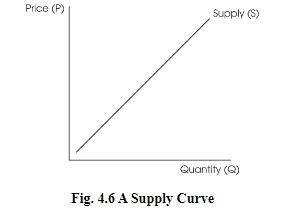

Supply and the Law of Supply

Quantity Supplied: has a direct relationship with changes in the price of a particular good

Since price has a different impact on both buyers and sellers, the supply curve is different than a demand curve

The market supply shows the quantity a supplier is willing and able to offer at various prices at a given time

The law of supply states that when prices increase, the supply increases as well (direct relation)

Reasons for the Law of Supply

Rising prices give greater opportunities to suppliers to earn a profit

With every additional unit, suppliers face an increase in the marginal cost of production

Charging higher prices provides them with the easiest way to cover the cost

The vice versa is also true; lower prices wouldn’t provide the incentive to motivate the supplier and thus reduces the quantity of product

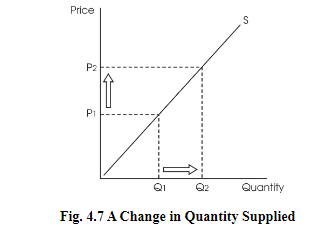

Change in Quantity Supplied vs. Change in Supply

Change in quantity supplied only takes place when price change takes place

As price increases (P1-P2), the quantity supplied also increases from Q1 to Q2. The change occurs along the supply curve

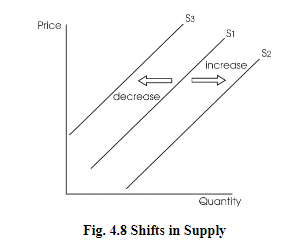

Shift in supply is due to the determinants of supply

Determinants of supply are the factors that influence the supplier to offer more or fewer goods at the same price

DETERMINANTS OF SUPPLY

Resource costs and availability

The cost of production (land, labor, capital) has an inverse impact on the supply

When the cost of these increases, the supplier decides to produce less of the products since he is unable to afford the production cost

Other goods and services

Suppliers who produce more than one product (profit-maximizing firms) have an easier time switching to the production of another product if issues do arise in prices

Technology

Newer technology causes the cost of production to decline and helps improve the efficiency of the supplier

This allows the supplier to produce more, shifting the supply curve outwards(toward right)

E.g. machines on the production line help reduce unit costs due to which more products are affordable by the supplier

Taxes and Subsidies

Taxes are added up to the unit cost of production, thus making it more expensive

Due to this, heavily taxed products are produced in less quantity by suppliers(supply curve shifts towards left)

Subsidies are the opposite of taxes and help reduce price per unit

This allows suppliers to produce more of the product(supply curve shifts towards the right)

Expectation

If suppliers expect prices to increase in the future, they would hold back supply for the current time with the future goal of earning more profit later (and vice versa)

Number of sellers

As the number of sellers increases in the market, the supply automatically increases

This allows consumers more choices at a lower price due to an increase in competition

MARKET EQUILIBRIUM: SUPPLY AND DEMAND TOGETHER

The market equilibrium price is that price which the market sets, where buyers buy the exact amount which the sellers are willing to produce. It’s also known as market-clearing price

The Equilibrium Price: price at which quantity supplied equals quantity demanded

A surplus would only exist when the quantity supplied is greater than the quantity demanded

A shortage would only exist when the quantity demanded is greater than the quantity supplied

In a competitive market where a surplus exists, prices eventually fall back to the equilibrium

In a competitive market where a shortage exists, prices eventually get pulled back up to equilibrium. This is because the shortage creates more demand from buyers

The suppliers utilize this and supply more at higher prices, thus bringing prices back up

Disequilibrium:This occurs when there is a shortage or surplus in the market. This surplus is what creates market disequilibrium

Changes in Equilibrium

Supply increases towards the right and decreases towards left

Demand increases towards the right (moves upwards) and decreases towards the left (moves downwards)

Just shift it, noting your new equilibrium price and quantity

General Rules:

When supply is constant and only demand increases, equilibrium price and quantity increases

When supply is constant and only demand decreases, equilibrium price and quantity decreases

When demand is constant and only supply increases, equilibrium price and quantity decreases

When demand is constant and only supply decreases, equilibrium price and quantity increases

The Double-Shift Rule

Double-shift rule: This rule states that when there is a simultaneous shift in both demand and supply, either price or quantity would stay indeterminate