Chapter 3 - Supply & demand

Buyers and sellers in markets

Market: market for any good consists of all buyers and sellers of that good.

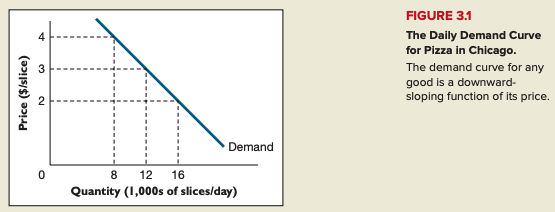

Demand curve: schedule/graph showing the quantity of a good that buyers wish to buy at each price.

Substitution effect: change in the quantity demanded of a good that results because buyers switch to or from substitutes when the price of the good changes.

Income effect: change in the quantity demanded of a good that results because a change in the price of a good changes the buyer's purchasing power.

Buyer's reservation price: the largest dollar amount the buyer would be willing to pay for good.

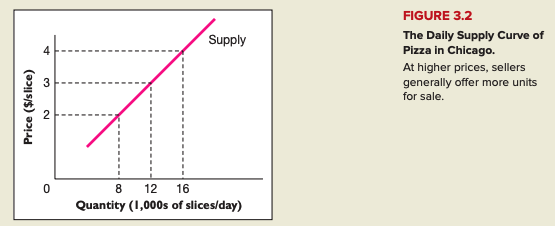

Supply curve: graph/schedule showing the quantity of a good that sellers wish to sell at each price.

Seller's reservation price: the smallest dollar amount for which a seller would be willing to sell an additional unit, generally equal to marginal cost.

Market equilibrium

Equilibrium: balanced/unchanging situation in which all forces at work within a system are canceled by others.

Equilibrium price and equilibrium quantity: price and quantity at the intersection of the supply and demand curves for the good.

Market equilibrium occurs in a market when all buyers and sellers are satisfied with their respective quantities at the market price.

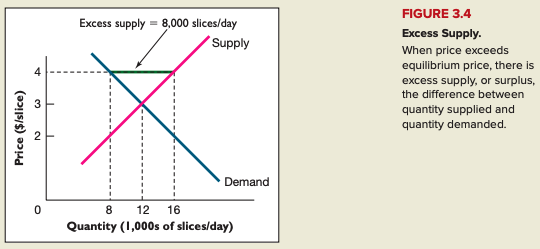

Excess supply: amount by which quantity supplied exceeds quantity demanded when the price of a good exceeds the equilibrium price.

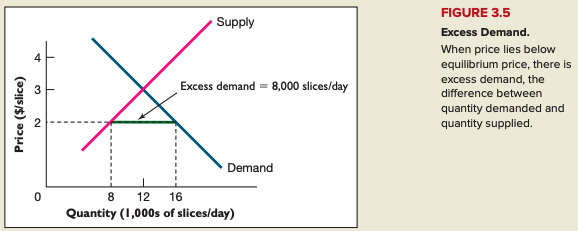

Excess demand: amount by which quantity demanded exceeds quantity supplied when the price of a good lies below the equilibrium price.

Predicting and explaining changes in prices and quantities

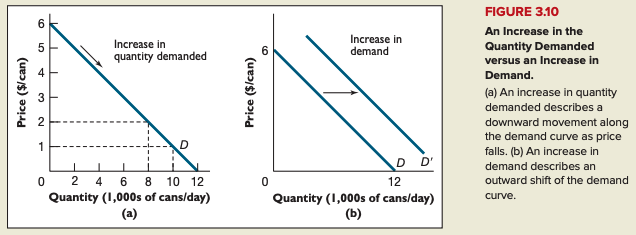

Change in the quantity demanded: movement along the demand curve that occurs in response to a change in price.

Change in demand: shift of the entire demand curve.

Change in the quantity supplied: movement along the supply curve that occurs in response to change in price

Change in supply: shift of the entire supply curve.

Complements: 2 goods are complements in consumption if an increase in the price of one causes a leftward shift in the demand curve for the other (or if a decrease causes a rightward shift).

Substitutes: 2 goods are substitutes in consumption if an increase in the price of one causes rightward shift in the demand curve for the other (or if a decrease causes a leftward shift).

Normal good: good whose demand curve shifts rightward when the incomes of buyers increase and leftward when the Incomes of buyers decrease.

Inferior good: good whose demand curve shifts leftward when the incomes of buyers increase and rightward when the incomes of buyers decrease.

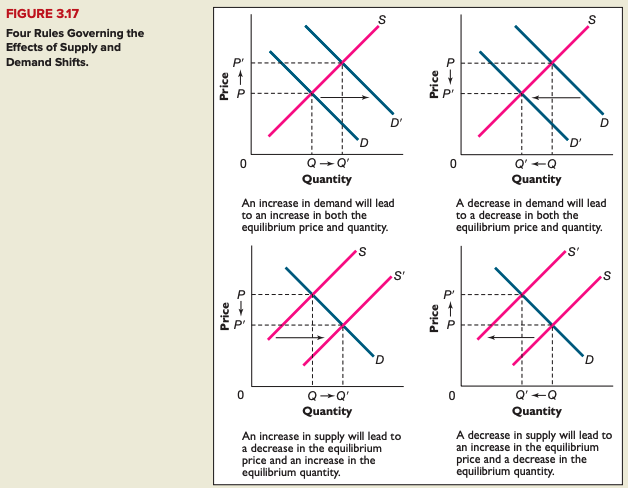

4 simple rules:

Factors that cause an increase (rightward/upward shift) in demand:

Decrease in the price of complements to the good/service

Increase in the price of substitutes for the good/service

Increase in income (for a normal good)

Increased preference by demanders for the good/service

Increase in the population of potential buyers

Expectation of higher prices in the future.

→ When these factors move in the opposite direction, demand will shift left.

Factors that cause an increase (rightward/downward shift) in supply:

Decrease in the cost of materials, labor or other inputs used in the production of the good/service

Improvement in technology that reduces the cost of producing the good/service

Improvement in the weather (especially for agricultural products)

Increase in the number of suppliers

Expectation of lower prices in the future.

→ When these factors move in the opposite direction, supply will shift left

Efficiency and equilibrium

Buyer's surplus: difference between the buyer's reservation price and the price he/she actually pays.

Seller's surplus: difference between the price received by the seller and his/her reservation price.

Total surplus: difference between the buyer's reservation price and the seller's reservation price.

Cash on the table: economic metaphor for unexploited gains from exchange.

Socially optimal quantity: quantity of a good that results in the maximum possible economic surplus from producing and consuming the good.

Efficiency = economic efficiency: condition that occurs when all goods and services are produced and consumed at their respective socially optimal levels.