Microeconomics

Microeconomics is focused with the behaviour of households, consumers, firms and resource owners, who are the most important economic decision-makers in a market economy.

Markets

Any kind of arrangement where buyers and sellers of goods, services or resources are linked together to set quantity and price.

Competitive Markets

Markets are considered free or competitive to the extent that private individuals and firms can openly attempt to win business away from each other in the hopes of earning greater profits.

Firms

An individual or organization that combines the factors of production to create and sell goods and services on the market.

Industry

An industry is made up of all the firms engaged in the same market activity.

Types of market structure

perfect competition

monopolistic competition

oligopoly

monopoly

Four Major Criteria for Market Structure

The number of firms in the industry.

A firm's level of market power.

The degree of product differentiation between goods offered by different firms.

The ease of exit and entry.

Perfect competition

Many firms in the industry

No individual influence on market

Identical products

Easy exit/entry

e.g. raw cocoa beans

Monopolistic competition

Many firms

No single firm can influence market price

Relatively differentiated products

Relatively easy exit/entry

e.g. restaurants, food trucks,clothing stores

Oligopoly

Handfull of firms

Significant control over price

Intyerdependent competition

High barriers to exit/entry

e.g; starbucks, dunkin, costa, tim hortons,

Duopoly

Only 2 firms dominate

Control most of market

Similar products

High barriers to exit or enter

e.g; boeing + airbus

Monopoly

Only 1 firm in market

Controls all output price

Only 1 type of product

Almost impossible to enter and exit

e.g; local monopolies on water & power

Monopsonist

Firm is single buyer in market

1 firm provides most employment in small cities

Hard for smaller suppliers to compete

Demand

The demand of an individual consumer indicates the various quantities of a good (or service) the consumer is willing and able to buy at different possible prices during a particular time period, ceteris paribus.

Quantity demanded

The quantity demanded can be referred to as the consumers’ intent for acquiring a specific amount of goods and services at a particular price.

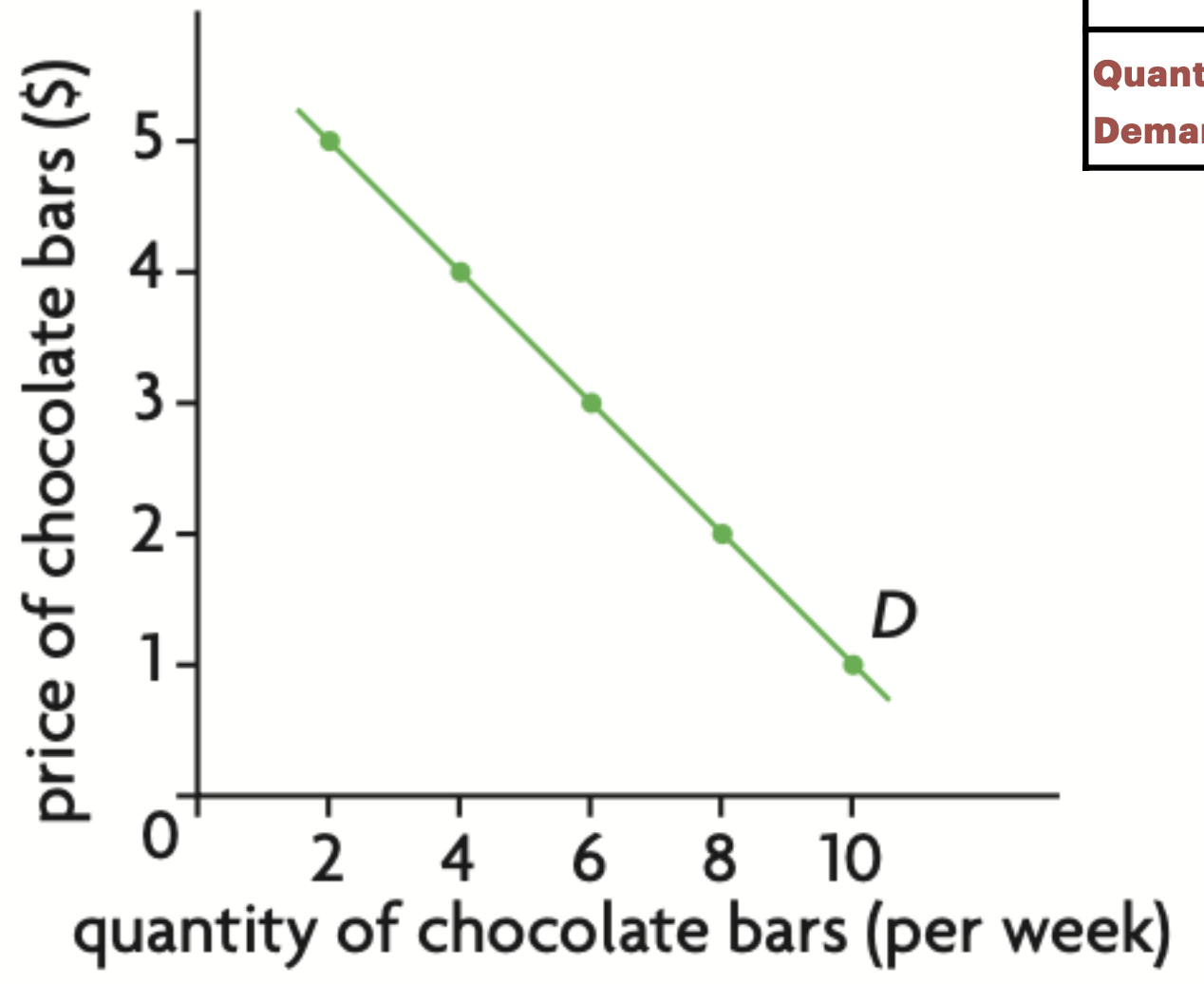

The demand curve

Law of demand

There is a negative causal relationship between the price of a good and its quantity demanded over a particular time period, ceteris paribus:

as the price of the good increases, quantity demanded falls; as the price falls, quantity demanded increases, ceteris paribus.

Why The Demand Curve Slopes Downward

Consumers buy goods and services because these provide them with some benefit, or satisfaction, also known as utility.

The extra benefit provided by each additional unit increases by smaller and smaller amounts. The extra benefit that you get from each additional unit of something you buy is called the marginal benefit or marginal utility.

Law of diminishing marginal utility

Utility is the extra satisfaction that one receives from consuming a product.

Marginal means extra.

Diminishing means decreasing.

Types of Goods

Free Goods.

Economic Goods.

Normal Goods.

Inferior Goods.

Giffen Goods.

Veblen Goods.

Final / Consumer Goods.

Capital Goods.

Intermediate Goods.

Raw Materials

Free goods

A free good is infinitely abundant and thus does not incur any opportunity costs in its production. e.g. air

Economic good

An economic good is a good which uses scarce resources in being provided and thus there is an opportunity cost of the alternative goods foregone.

Normal goods

Affected by level of household income

As salary increases, consumption increases

most goods are normal

Inferior goods

Affected by level of household income

As salary decreases, consumption increases

e.g. bus tickets, 2nd hand clothing

Giffen goods

Like an inferior good → as income falls, demand rises

Irreplaceable good (poor people budget)

Claimes a large portion of consumers’ budget

as price increases, demand increases

Bread/rice in poorer areas

Veblen goods

Veblen: ostentatious, showy, flamboyant

To show purchasing power & status

higher price = higher demand

e.g; Birkin bag

Capital goods

Good purchased to serve a purpose of production/service for company

Used to produce the good

e.g; printer to print papers for ads

Intermediate goods

Raw materials used to produce another product or service

Used in the product

e.g; steel used to make cars

Consumer/final goods

End product that businesses sell directly to consumers

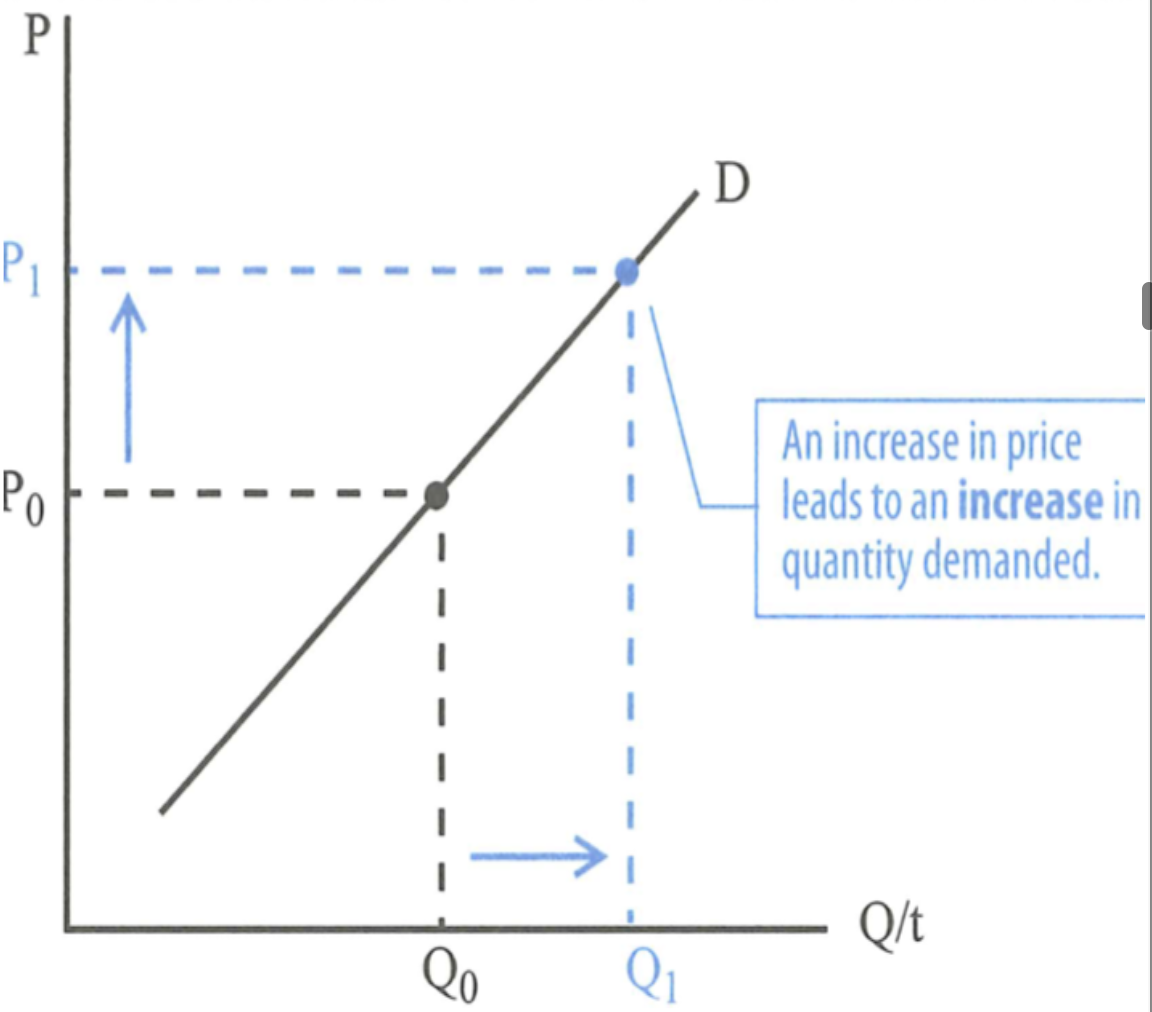

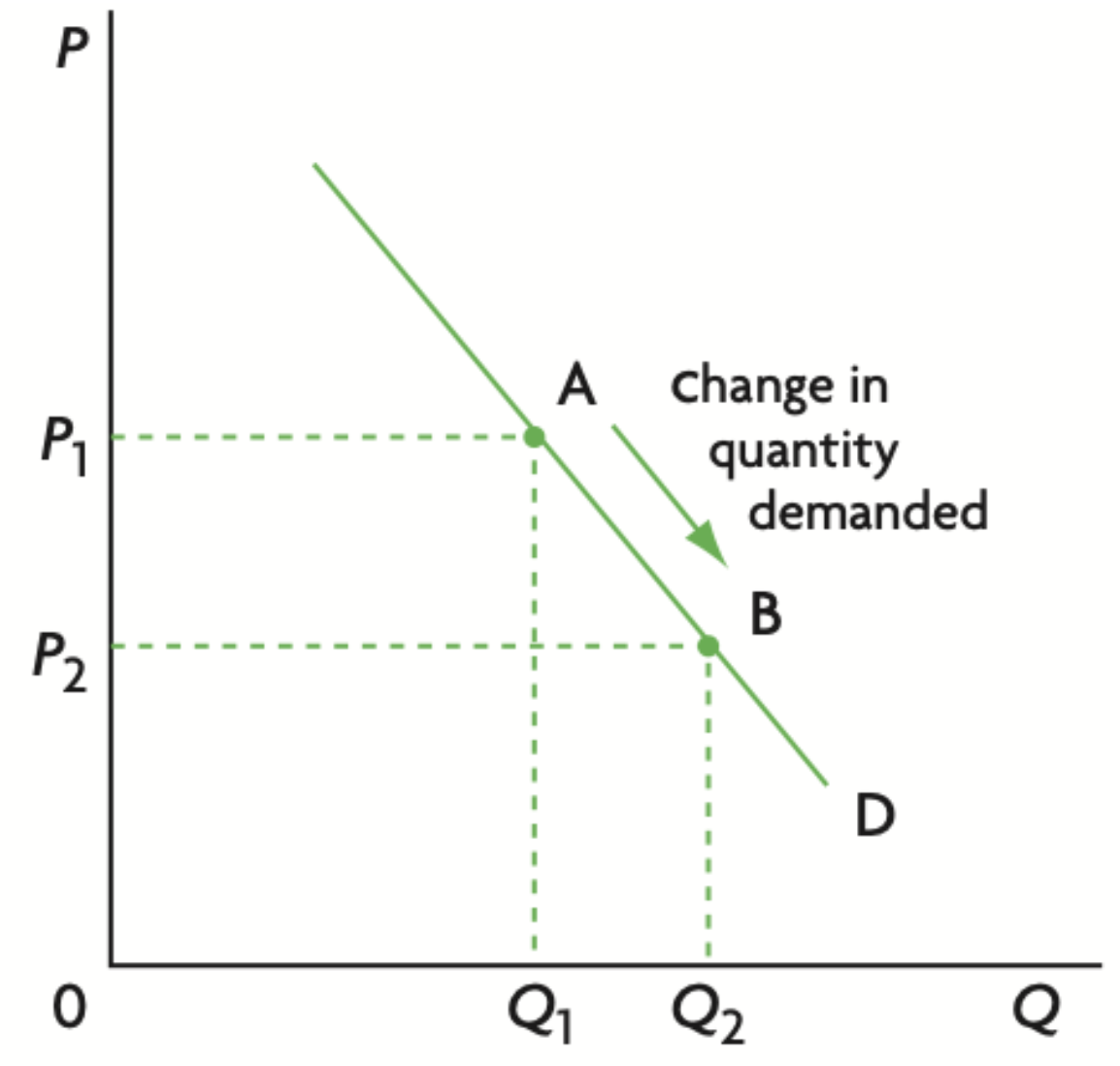

Effect of price on demand

Whenever the price of a good changes, ceteris paribus, it leads to a movement along the demand curve.

If the price falls from P1 to P2, the quantity of the good demanded increases from Q1 to Q2

Income effect

A fall in price = people demanding are “richer” because their income can buy more of the good → more likely to increase consumption

Substitution effect

Fall in price of a good = price of alternative (substitute) good to increase (relatively)

Consumers will substitute other goods with the lower priced good.

Non-price Determinants of Demand (NPD)

Income in the case of normal goods.

increase income = increase demand

Income in the case of inferior goods.

increase income = decrease demand

Preferences and tastes.

when goods become favourable/popular, people want more

Prices of substitute goods.

price of substitute goods increases = demand of initial goods increases

Prices of complementary goods (Derived Demand).

Goods that tend to be used together; e.g smartphone & charger.

price of 1 good falls, demand of other increases (mutually affect each other)

Demographic (population) changes implying changes in the number of buyers.

increased # of buyers = increase market demand

Expectations of Consumers

When people predict things

If future prices expected to rise, demand now increases

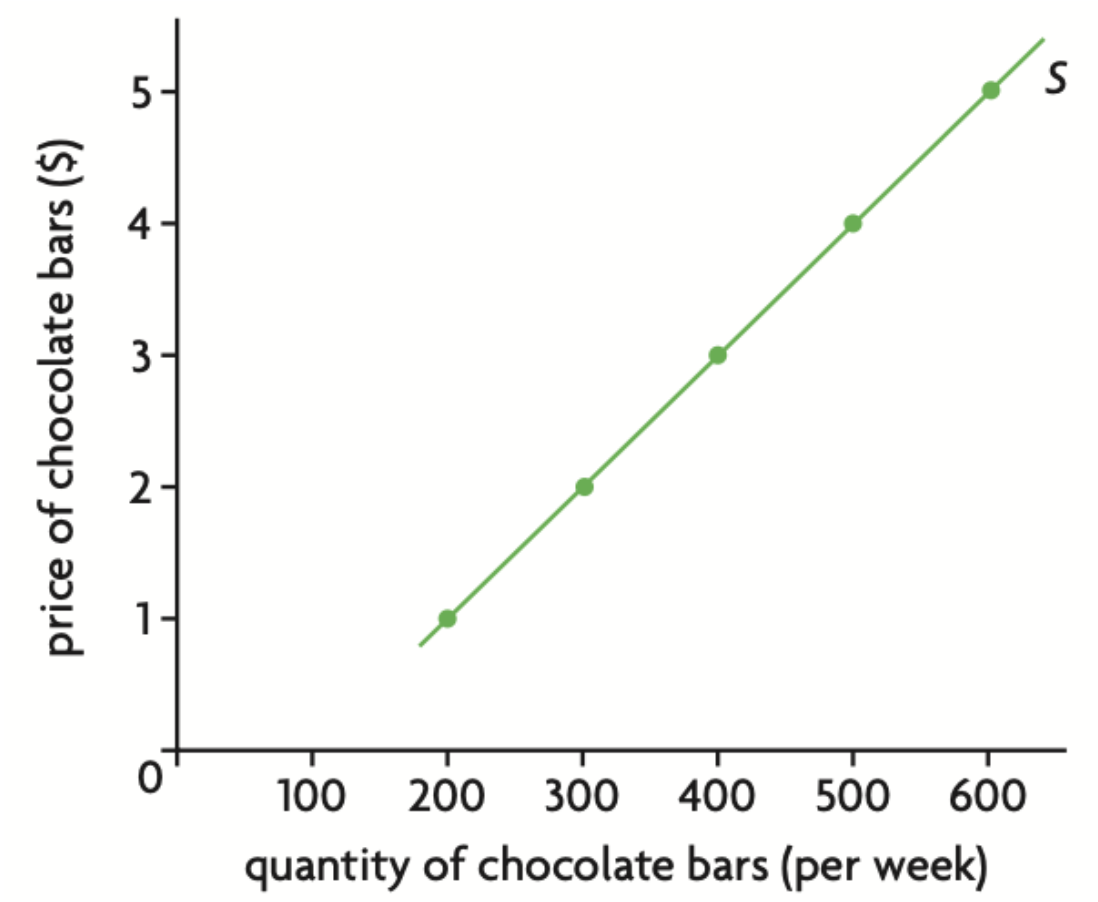

Supply

The supply of an individual firm indicates the various quantities of a good (or service) a firm is willing and able to produce and provide to the market for sale at different possible prices, during a particular time period, ceteris paribus.

QUantity supplied

Quantity supplied describes the number of goods or services that suppliers will produce and sell at a given market price.

The supply curve

LAw of supply

There is a positive causal relationship between the quantity of a good supplied over a particular time period and its price.

As the price of the good increases, the quantity of the good supplied also increases; as the price falls, the quantity supplied also falls, ceteris paribus.

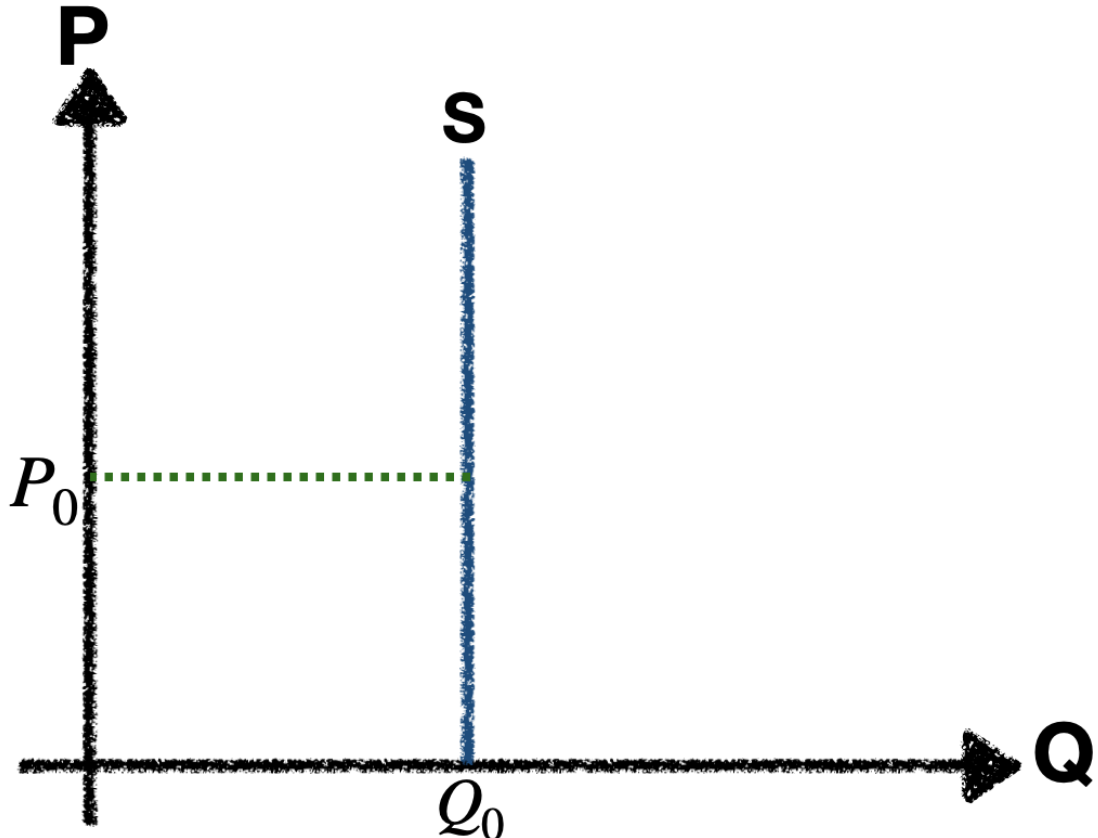

Vertical supply curve

Even as price increases, the quantity supplied cannot increase; it remains constant. There is a fixed quantity of the good supplied because:

There is no time to produce more of it.

There is no possibility of ever producing more of it.

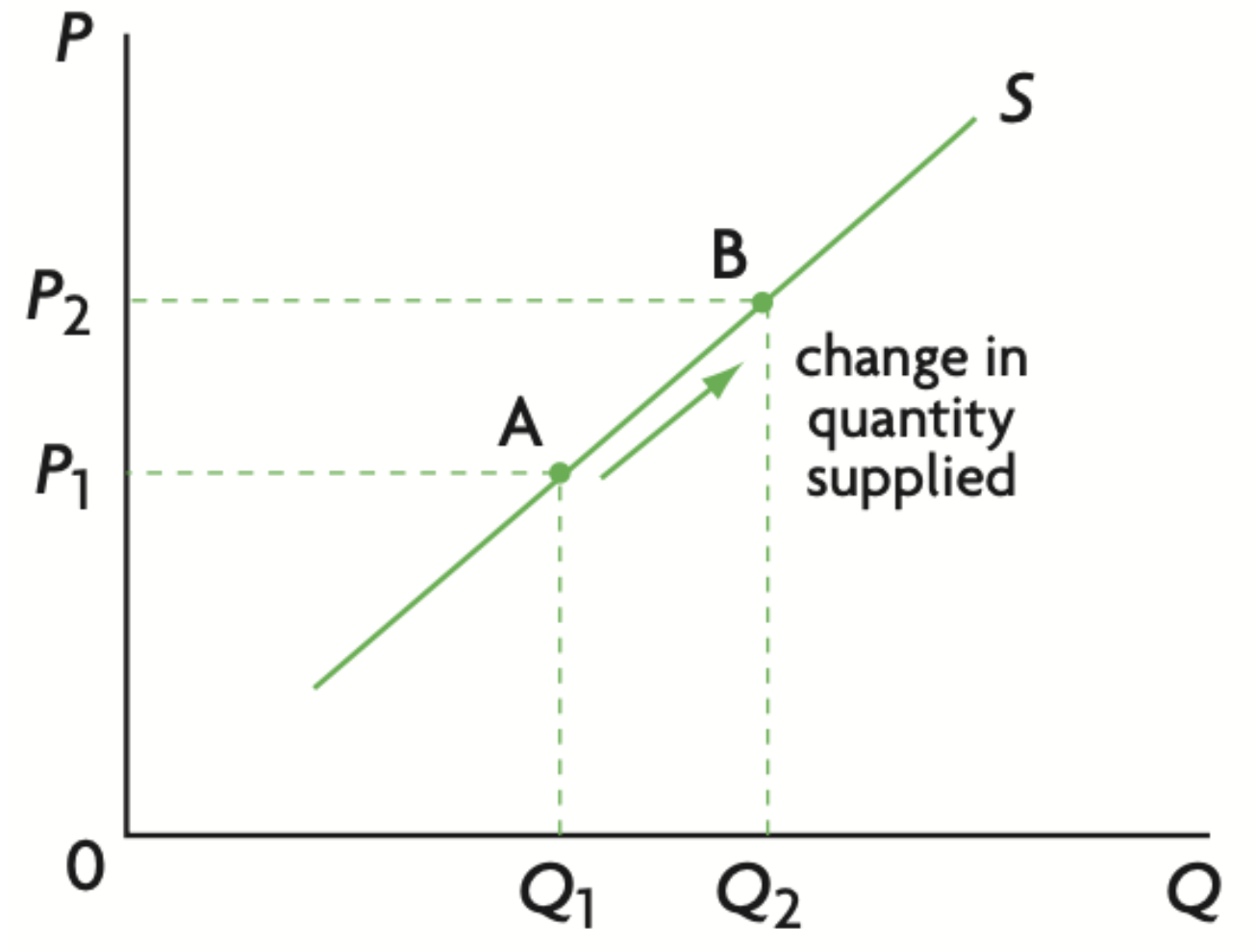

Effect of price on supply

Any change in price produces a change in quantity supplied, shown as a movement on the supply curve.

Any change in a determinant of supply (other than price) produces a change in supply, represented by a shift of the whole supply curve.

Non-price Determinants of Supply

Costs of factors of production.

Factors of production increase = supply decrease

Technology.

More improved technology = lower cost of production = supply increase

Prices of related goods: competitive supply.

Firms competing for same resources

Firm producing more of 1 good = other firm must produce less of other

Prices of related goods: joint supply.

Production of goods derrived from single product, e.g. milk + beef

More supply of 1 product = more of other product

Producer/firm expectations.

If prices expected to rise in future, firms will withhold products from market to sell at higher prices later

Taxes (direct or indirect taxes).

Taxes increase = supply decrease

Subsidies.

Subsidies increase = supply increase

The number of firms.

# firms increase = total supply increase

‘Shocks’, or sudden unpredictable events.

Affected production costs = affect supply

e.g. war, pandemic, disaster

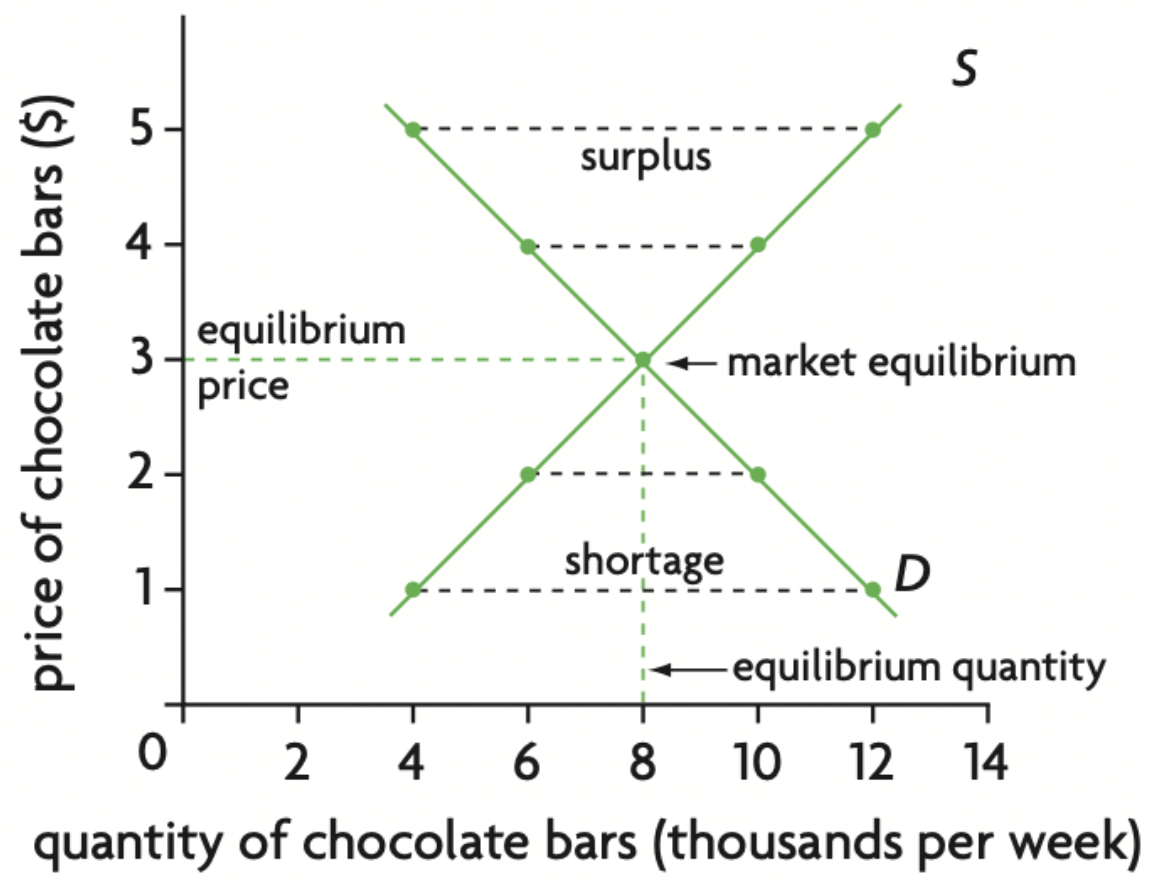

Market equilibrium

When a market is in equilibrium, quantity demanded equals quantity supplied, and there is no tendency for the price to change. In a market disequilibrium, there is excess demand (shortage) or excess supply (surplus), and the forces of demand and supply cause the price to change until the market reaches equilibrium.

Surplus VS shortage in a market

If quantity demanded of a good is smaller than quantity supplied, the difference between the two is called a surplus, where there is excess supply.

If quantity demanded of a good is larger than quantity supplied, the difference is called a shortage, where there is excess demand.

Invisible hand in a market

Individuals are guided by a price. When consumers act in best self-interest, they benefit the market

Price Acts as Signals & Incentives

Price communicates information to decision-makers: incited consumers to respond accordingly

high price = shortage of supply = producers need to produce more

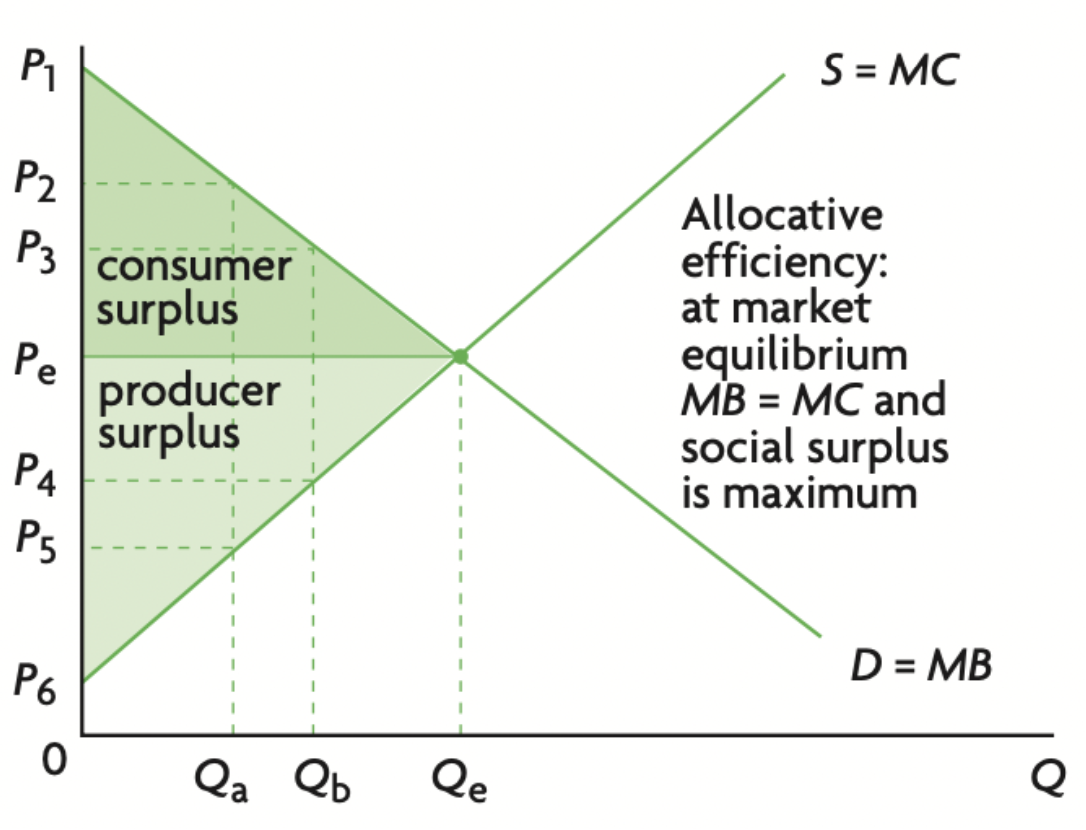

Consumer surplus

Consumer surplus is defined as the highest price consumers are willing to pay for a good minus the price actually paid.

Allocative efficiency

At market equilibrium. The competitive market realises allocative efficiency, producing the combination of goods mostly wanted by society, thus answering the what to produce question in the best possible way.

Productive efficiency

Productive efficiency is production with the fewest possible resources, thus answering the how to produce question in the best possible way.

Producer surplus

The price received by firms for selling their good minus the lowest price that they are willing to accept to produce the good.

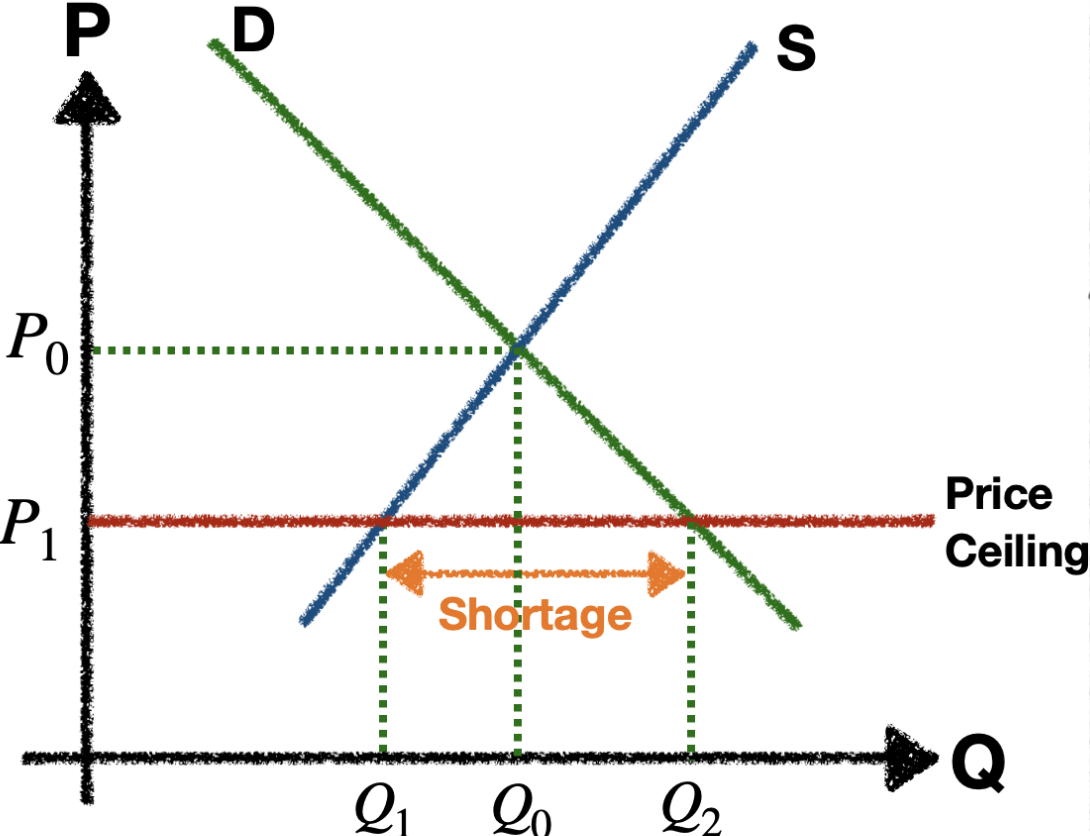

Price controls

governing body has market interventions by controlling prices on non-clearing markets: excess of supply or excess of demand

Price ceiling

Price ceiling is a price set down in law that the price of a good may not be set above a certain level.

Often these are imposed to make basic goods & services more affordable for poorer households; e.g. staple foods like bread, rice, & grain, or rent control

Effects of price ceiling

Shortages & Decreased Market Size.

Demand > supply

Rationing.

Govt. supplies everyone equally. → barter deals: trade goods for other goods

Elimination of Allocative Efficiency.

maginal benefitt ≠ maginal cost

Informal/Black Markets.

Selling necesities at prices much higher than p1

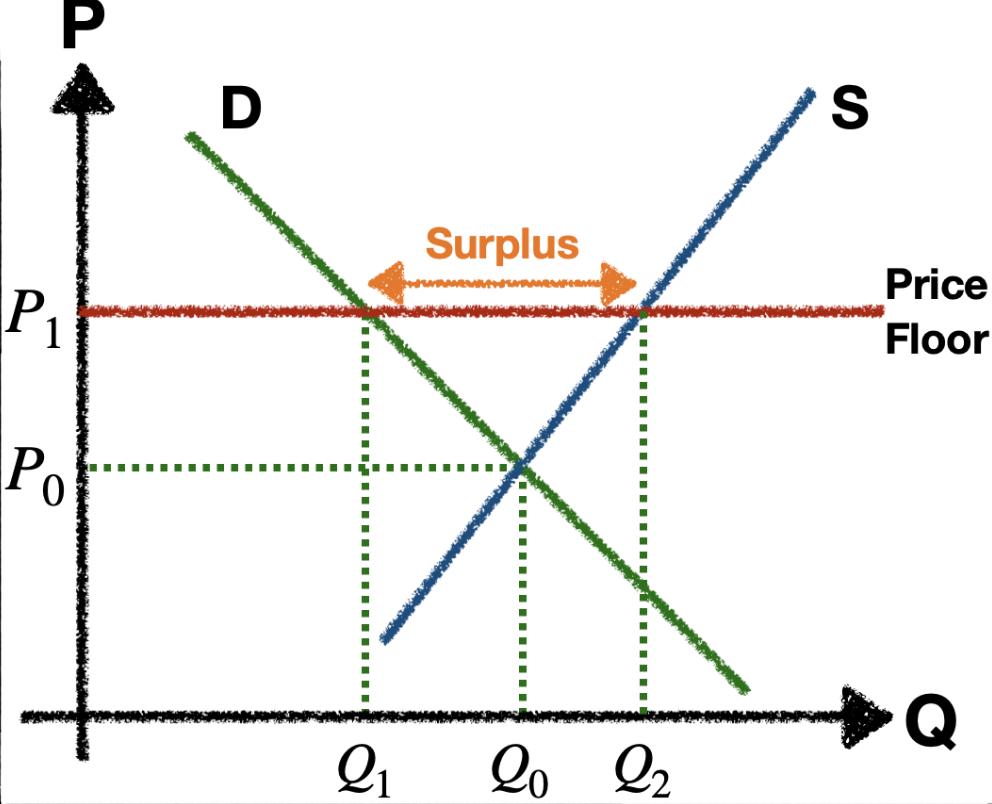

Price floor

A price set down in law that the price may not be set below a certain level.

May be supporting employment in a certain way

Effects of price floor

Surplus & Reduced Market Size.

demand < supply

Cost Inefficiency.

Higher-cost production is inefficient

Allocative Inefficiency.

Informal/Black Markets.

firms sell surplus at prices below equilibrium

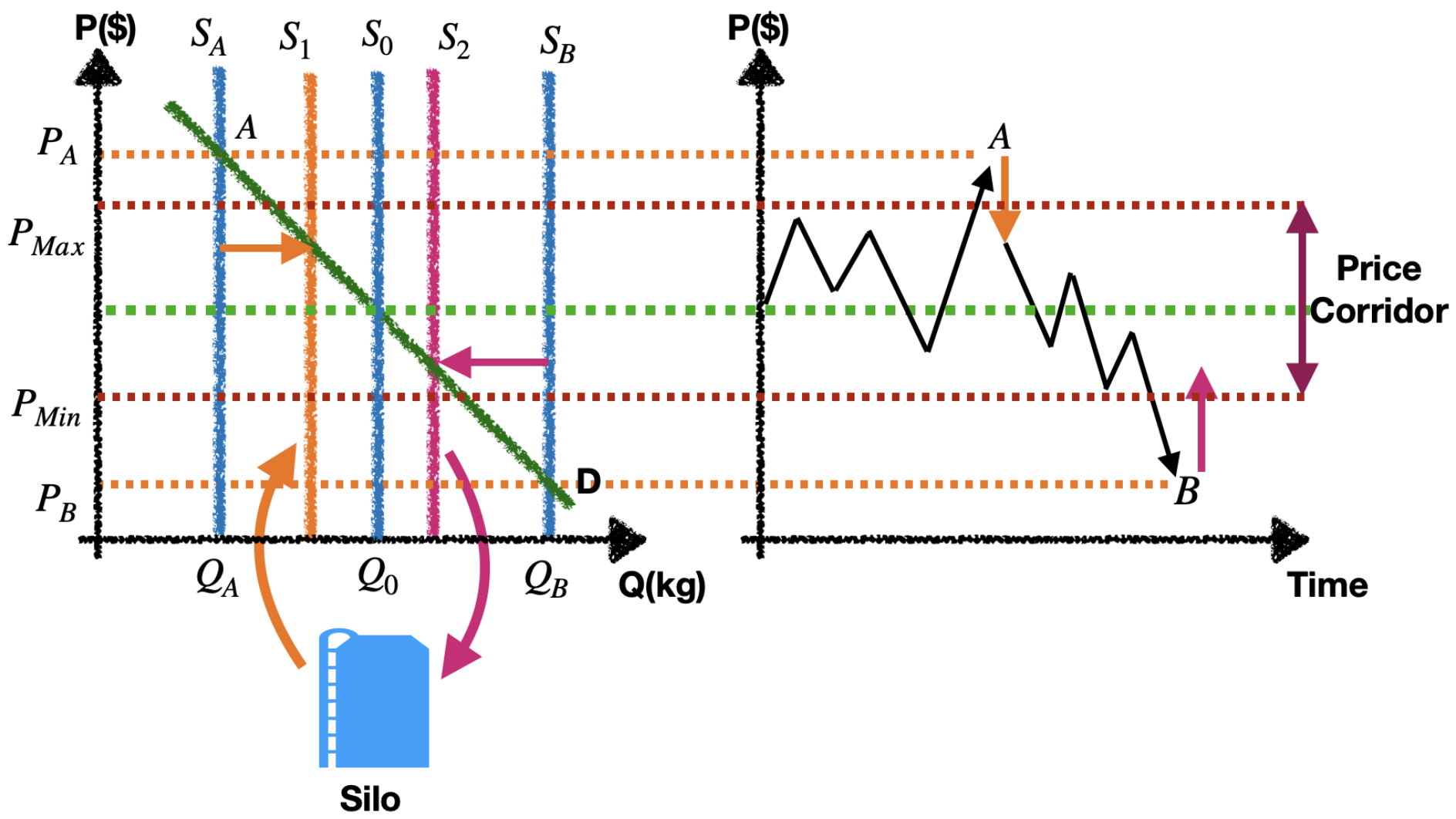

Buffer stocks

The purpose of a buffer stock scheme is to stabilise and uphold a certain price.

When demand is high, they increase supply; when demand is low, they store excess supply

The good has to be storable since it runs the risk of being stored for an indeterminate period.

The good is often a commodity, i.e. a primary good such as rubber, sugar, coffee and grain.

There are considerable price fluctuations on the market.

How buffer stocks work

International Commodity Agreements (ICA)

Allow members to use commodity agreements to influence world prices

Often govt. is very involved

within countries it’s illegal, intl. is legal

e.g; rubber, cocoa, petrol, etc.

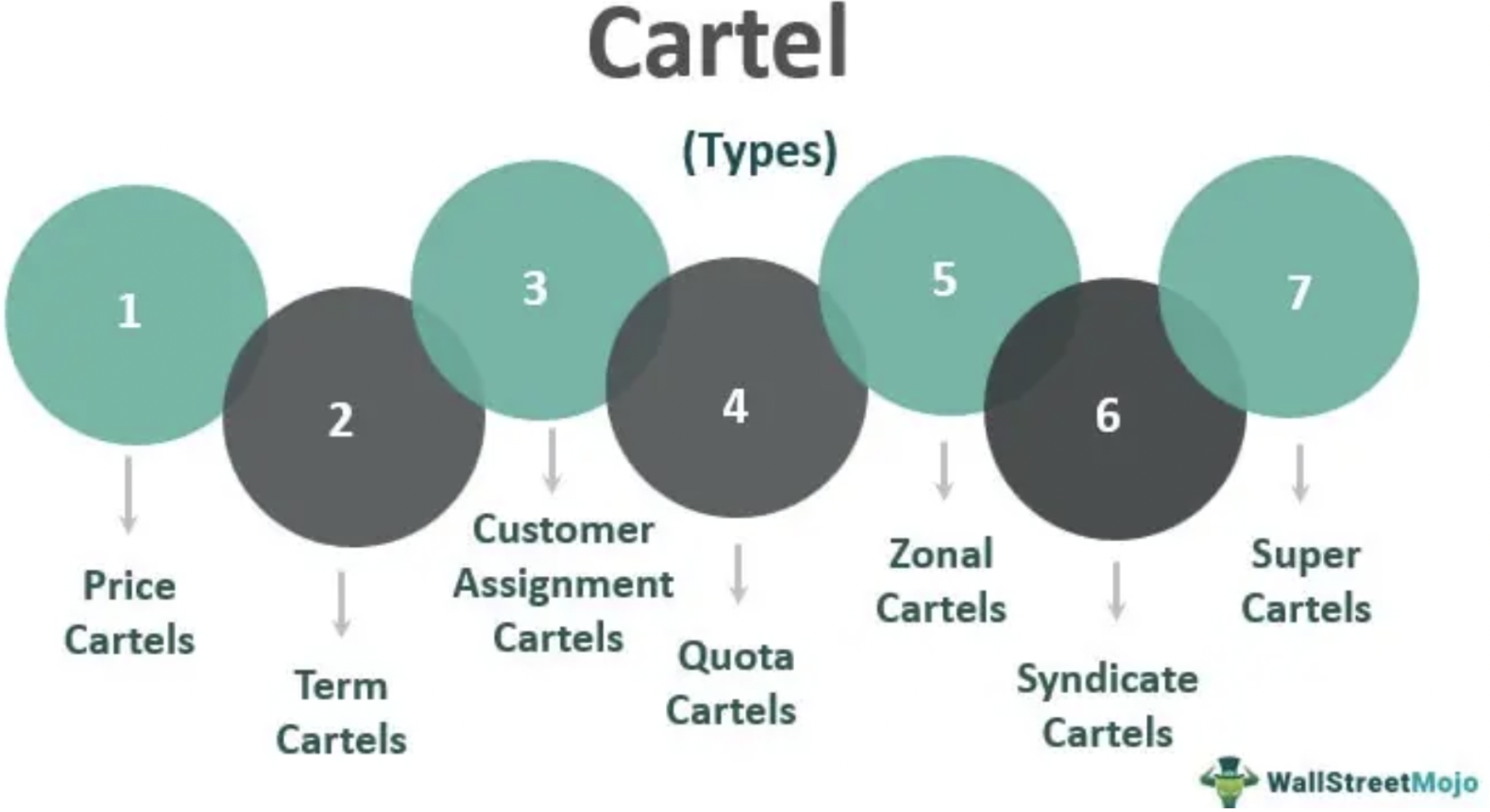

Cartel

A group of producers of goods or suppliers of services formed through an agreement amongst themselves, whether or not through a formal agreement in writing, to regulate the supply of goods or services with the basic intent to control the prices illegally or to restrict competition in respect of the said goods or services.

Cartel types

price cartels

Term cartels: create term agreements to form alliance

Customer assignment cartels: each comapny is assigned specific customer demographic

Quota cartels: e.g. OPEC, regulate how much each producer can produce

Zonal cartels: dividing country into zones so each company only in specific zone

Syndicate cartels: Drug cartels: crimes

Super cartels: Large cartels